By the MIA Capital Market and Assurance Team

In response to the growing demand for sustainability information, the International Ethics Standards Board for Accountants (IESBA) officially launched the International Ethics Standards for Sustainability Assurance (IESSA) in January 2025. This landmark development addresses the increasing need for global ethics and independence standards that promote transparency and reliability in sustainability reporting and assurance.

The Institute, in its feedback during the exposure draft phase, expressed support for the development of ethics standards in relation to sustainability assurance as a global benchmark and viewed this development as pivotal to enhancing consistency in practices and building trust in sustainability information. Nevertheless, the response also noted that putting these standards into practice is not without its challenges.

Read the Institute’s response to the exposure draft of the IESSA in full here.

Key features of the finalised IESSA

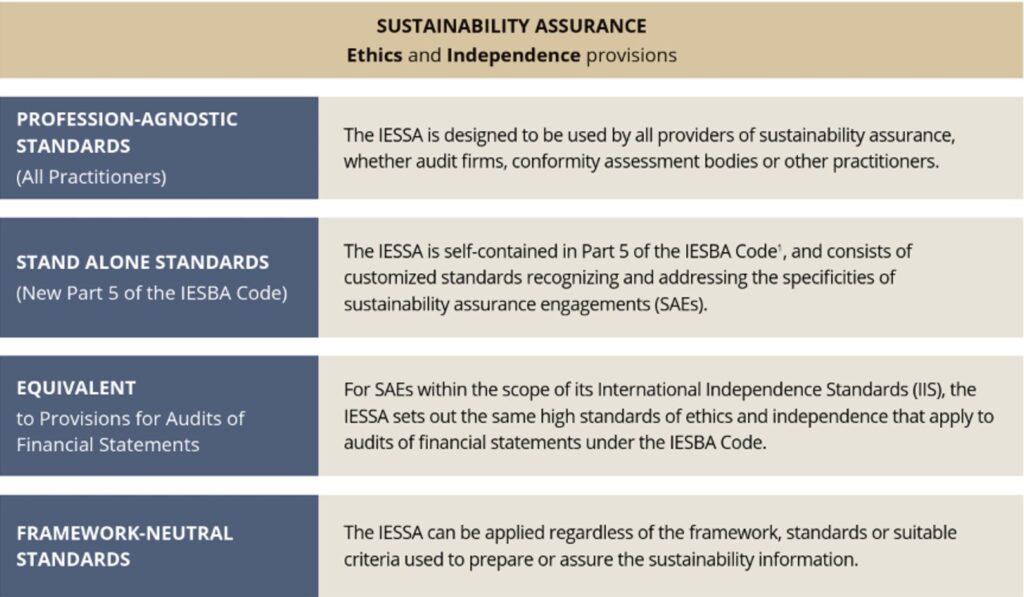

The IESSA introduces a new Part 5 to the Code of Ethics which is framework-neutral and profession-agnostic. This ensures its applicability to all sustainability assurance practitioners, regardless of whether they are professional accountants.

Figure 1: Key features of the IESSA

Source: Technical Overview: International Ethics Standards for Sustainability Assurance (IESSA)

The finalised standard builds on many of the core principles found in ethics and independence standards for financial statement audits but includes tailored revisions for sustainability assurance engagements. These include:

- Sustainability-specific examples of threats and safeguards.

- Independence considerations when assurance work is performed at value chain entities.

- Provisions addressing group sustainability assurance engagements.

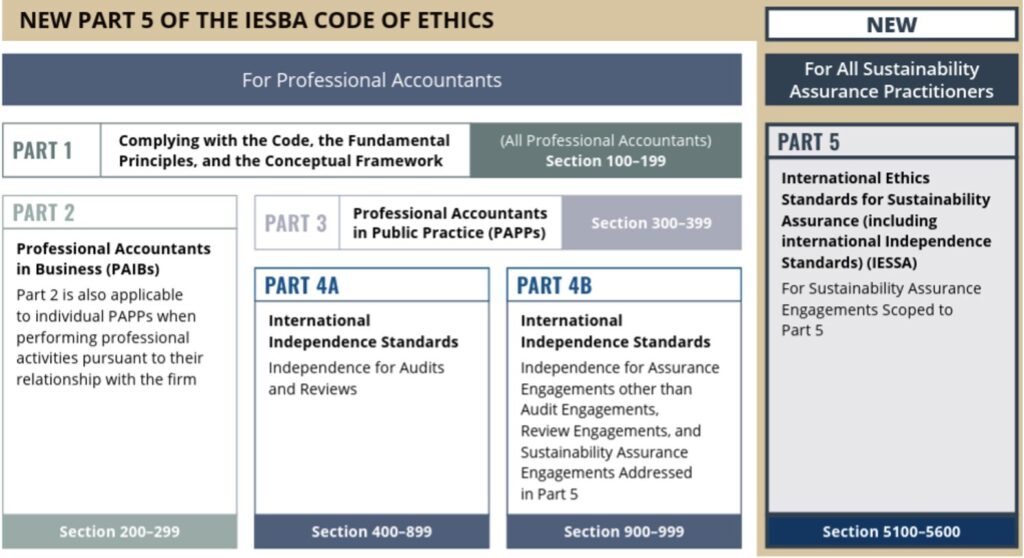

Additionally, updates to Parts 1–3 of the Code of Ethics for professional accountants were introduced. These updates incorporate references to sustainability, which are particularly relevant for those involved in sustainability reporting. Key areas of focus include conduct to mislead or intent to mislead in sustainability reporting (greenwashing), value chain considerations, and the forward-looking nature of sustainability information.

Figure 2: New Part 5 of the IESBA Code of Ethics

Source: Ethics & Independence for Sustainability Assurance – Fact Sheet, January 2025, IESBA

Revisions related to sustainability may seem limited for preparers at this point in time but the IESBA has since indicated in its 2024 – 2027 Strategy and Work Plan that it will explore the development of profession-agnostic standards for sustainability reporting beginning in 2025 as a key strategic area.

Alignment with ISSA 5000

The IESSA was developed in close collaboration with the International Auditing and Assurance Standards Board (IAASB) to ensure consistency with the International Standard on Sustainability Assurance (ISSA) 5000. Together, these standards establish a strong foundation for sustainability assurance practices globally and reinforce the importance of ethical behaviour and independence in sustainability reporting and assurance.

Implementation considerations

While the Institute supports the adoption of the IESSA, it acknowledges the challenges in achieving consistent application across diverse professional backgrounds. Practitioners already familiar with the existing Code of Ethics may find implementation more straightforward, while those who are not professional accountants may require additional training and guidance.

A key area of concern is the practical application of independence requirements to value chain entities. Since assurance clients do not have direct control over these entities, meeting independence requirements could be challenging.

To address these challenges, the IESBA will be providing support through webinars, implementation guidance and continued implementation monitoring and feedback channels to support implementation and consistent application.

What comes next

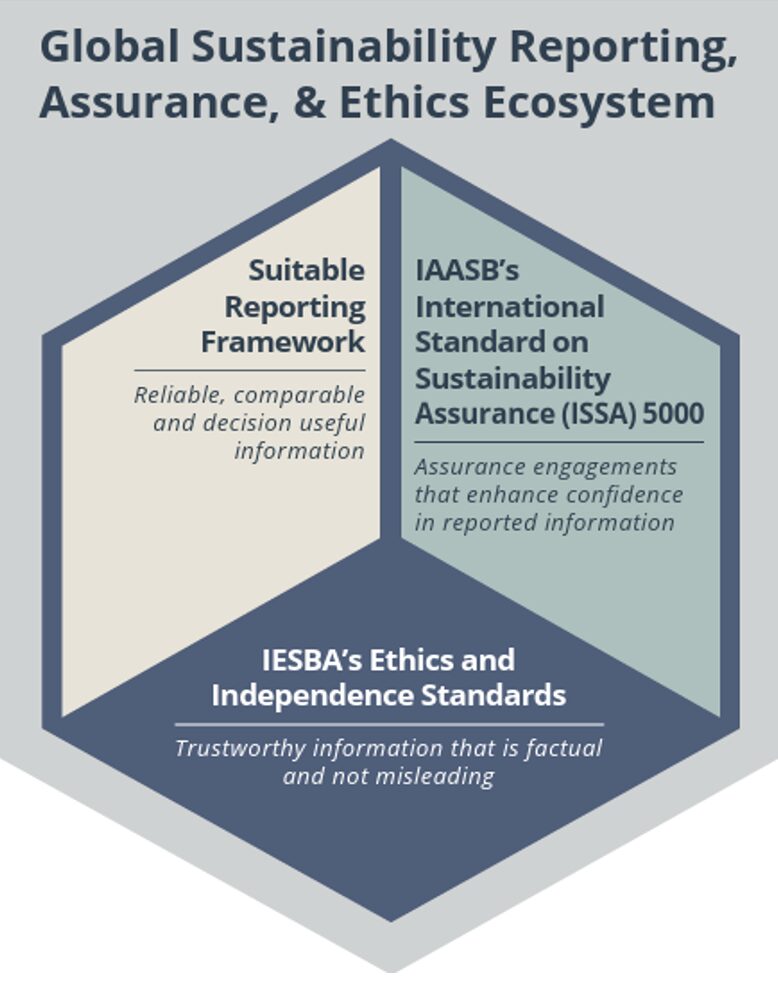

As jurisdictions around the world move to introduce mandatory sustainability reporting and assurance, the IESSA will play a key role in connecting these standards as the IESBA designed these standards to serve as a third pillar, complementing the existing reporting ecosystem along with the ISSA 5000. It reflects the understanding that ethical behaviour is imperative in ensuring the trustworthiness and integrity of sustainability information.

Figure 3: The sustainability reporting, assurance and ethics ecosystem

Source: ISSA 5000 and IESSA: Global Baseline Standards for Sustainability Assurance, January 2025, IESBA

At the national level, notable developments include Malaysia’s launch of the National Sustainability Reporting Framework (NSRF), which will guide the country’s strategy and approach in integrating sustainability into its regulatory and reporting landscape. The NSRF clarifies that the IFRS Sustainability Disclosure Standards issued by the International Sustainability Standards Board (ISSB) will be the baseline sustainability reporting standards for listed and large non-listed companies in Malaysia.

In addition, the Institute has also launched its Sustainability Blueprint for the Accountancy Profession in June 2024. The Blueprint strives to empower accountants to align their practices with sustainability imperatives with the following objectives:

- Establish aspirations for accountants in Malaysia with regard to sustainability

- Analyse key challenges facing the accountancy profession in Malaysia based on the domestic and global sustainability landscape

- Enable accountants in the sustainability space.

The Blueprint also underscores the importance of ethics as a fundamental pillar of the profession when addressing sustainability-related matters.

The IESSA not only highlights the growing importance of ethical standards in sustainability assurance but will also guide accountants in navigating the ethical challenges of this evolving landscape. The IESSA will be effective for sustainability assurance engagements on sustainability information for periods beginning on or after 15 December 2026, with transitional provisions. At present, the Ethics Standards Board of the Institute is assessing the implementation of these standards in Malaysia.

Learn more about the IESBA’s work on sustainability on their website here.