By Sustainability, Digital Economy and Reporting Team

Sustainability reporting plays a crucial role in helping the public sector meet its sustainability goals, aligning government efforts with broader environmental targets and enabling implementation of policies such as the National Climate Change Policy 2.0.

As a keen advocate for sustainability in business and the profession, MIA is committed to capacity and competency building in both the public and private sustainability reporting space. To advance its sustainability agenda, MIA launched the MIA Sustainability Blueprint for the Accountancy Profession in 2024, and has embarked on implementing the MIA Sustainability Roadmap (Roadmap).

A key initiative under the Roadmap was the recent webinar on Public Sector Sustainability Reporting: Where do We Stand? that was successfully held on 26 February 2025 and drew close to 500 MIA members. Moderated by Encik Mohamad Hamim, Executive Director, Project Management Kuala Lumpur City Hall and a member of the MIA Public Sector Accounting Committee (PSAC), the webinar featured valuable insights from Datuk Nor Yati binti Ahmad, Accountant General of Malaysia and Chair of PSAC, Datu Hajah Elean Masa’at, Sarawak Accountant General, and Puan Rasmimi Ramli, Executive Director, Sustainability, Digital Economy and Reporting of MIA.

The webinar kicked off with a presentation on the global updates of public sector sustainability reporting, followed by a panel discussion that highlighted the significance of transparency and accountability in public sector sustainability efforts. The panellists also discussed the impact of reporting on decision-making, policy development and public trust as well as the necessary steps to improve reporting practices in the future.

How Sustainability Reporting Benefits the Public Sector

According to Puan Rasmimi, sustainability reporting plays a crucial role in helping the public sector meet its sustainability goals, aligning government efforts with broader climate and environmental targets. Here are the key benefits:

- Increased Transparency and Accountability: Sustainability reporting enhances public sector transparency by providing clear disclosures on how sustainability risks and opportunities are managed which helps stakeholders, including citizens and investors, better understand how the government addresses its sustainability risks and opportunities.

- Integration with Financial Reporting: Unlike many standalone sustainability reporting frameworks, IPSASB Sustainability Reporting Standards (SRS) integrate seamlessly with existing financial frameworks, such as IPSAS (International Public Sector Accounting Standards). This integration offers a comprehensive view of both financial and sustainability performance, allowing for a holistic understanding by the primary users of general purpose financial reports.

- Alignment with Private Sector Standards: Public sector sustainability reporting standards align with private sector reporting standards such as IFRS S2 Climate-related Disclosures, enabling easier comparison of climate-related disclosures across both sectors. This alignment helps investors and policymakers make informed decisions.

- Evidence-Based Decision Making: Sustainability reporting generates essential data that governments can use to assess the effectiveness of their sustainability strategies. This data enables informed policy adjustments and more efficient resource allocation, driving impactful sustainability initiatives.

Supporting Malaysia’s Climate Goals Through Sustainability Reporting

Datuk Nor Yati highlighted the importance of sustainability reporting in supporting government efforts to implement climate policies under the National Climate Change Policy 2.0. It enables better climate governance, supports transitions to net zero, and supports informed budget planning through financial and non-financial insights. The integration with outcome-based budgeting also enhances transparency in how public funds are allocated for green initiatives such as renewable energy and disaster risk management.

“Sustainability reporting helps ensure transparency on how government resources are allocated towards climate initiatives,” said Datuk Nor Yati.

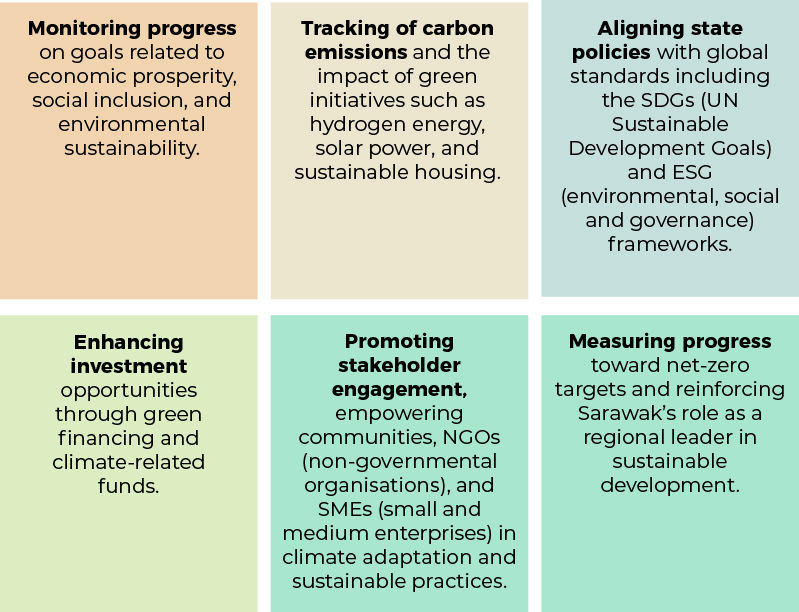

Sarawak’s Post COVID-19 Development Strategy 2030 (PCDS 2030)

The Post Covid-19 Development Strategy 2030, launched in 2021, serves as a roadmap for Sarawak to achieve prosperity, inclusivity and environmental sustainability by 2030. Environmental Sustainability is one of the seven strategic thrusts under PCDS 2030, being embedded in state-wide policies, guided by the Sarawak Sustainability Blueprint. Launched in October 2024, this comprehensive blueprint outlined 10 strategic thrusts which aims to guide the state towards a sustainable future, comprising energy transition, sustainable agriculture and food security, green mobility, circular economy, sustainable manufacturing, sustainable and responsible mining, protection and enhancement of natural assets, sustainable cities, community development and eco-tourism.

Sustainability reporting plays a key role in supporting this strategy by enabling:

“Sustainability reporting ensures our strategies are measurable, accountable and impactful,” said Datu Hajah Elean.

Navigating Challenges in Implementing Sustainability Reporting Standards

Datuk Nor Yati highlighted several key considerations in implementing sustainability reporting standards such as IPSASB SRS ED S1 Climate-related Disclosures. One is the availability and consistency of data, as sustainability-related information is often fragmented across ministries and may not yet be verified through assurance processes. She also noted the importance of building technical capacity, particularly in linking environmental data with financial implications. As this is a new and evolving area, gradual enhancement of skills, especially among public sector accountants, will be crucial.

“The challenge is how to relate all those data with the financial impact—our accountants need to shift from debit and credit to data analysis,” she explained.

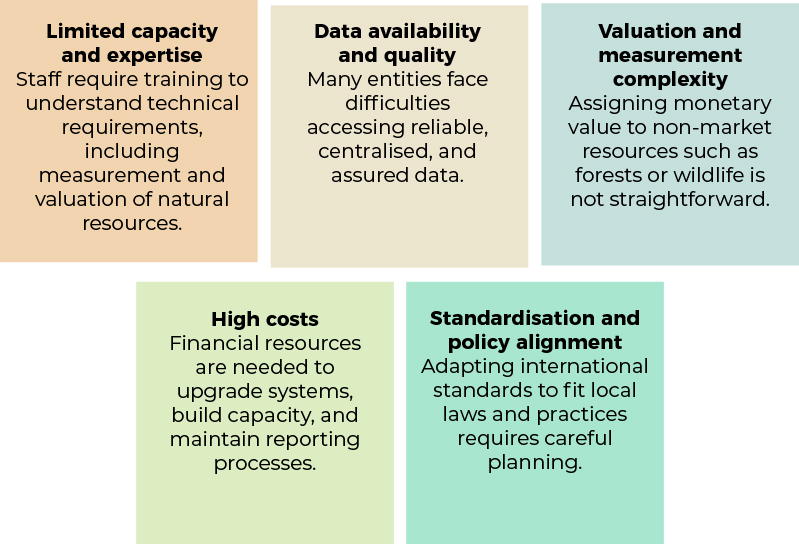

Datu Hajah Elean likewise outlined key challenges in implementing sustainability reporting standards.

The main challenges include:

“With the right commitment and collaboration, these challenges can become opportunities to build stronger, more transparent reporting,” said Datu’ Hajah Elean, emphasising the potential for long-term improvement.

She further underscored the need for cross-sector coordination, legal and policy alignment, and stronger community engagement to support a successful transition toward sustainability reporting.

IPSASB SRS ED 1: Guiding Public Sector Entities Towards Climate Reporting

Puan Rasmimi highlighted how IPSASB SRS ED 1 supports public sector entities in preparing for climate reporting, as outlined below:

- Structured Guidance: The ED is systematically organised beginning with scope and definitions, followed by a step-by-step guide, including a decision flowchart that helps entities determine if they should report on their operations, public policy programmes, or both. It then guides entities on the four pillars of climate-related disclosure—governance, strategy, risk management, and metrics & targets—with application guidance and illustrative examples.

- Determining Material Information: The ED outlines a three-step approach to identify material information:

- Understand the entity’s context – understand its own activities, relationships, and stakeholders, as well as the broader sustainability context, including national targets and commitments to which a subnational entity contributes.

- Identify actual and potential outcomes, risks, opportunities – identify climate-related risks and opportunities to the entity’s operations and assess the actual intended and unintended outcomes of its climate-related public policy programmes.

- Determine material information – based on the broad identification of outcomes, risks and opportunities, determine what information is material for its primary users. Materiality requires judgments about information from a quantitative and qualitative perspective and will be unique to each entity.

- Understand the Entity’s Transitional Provisions: To ease adoption, the ED includes transitional measures to help entities address implementation challenges.

“The ED provides a thoughtful, practical approach that supports public sector entities in making informed, context-specific climate disclosures,” she remarked.

Private Sector – Navigating Sustainability Reporting Through Phased Implementation

In addressing the private sector’s progress under the National Sustainability Reporting Framework (NSRF), Puan Rasmimi explained that many of the challenges faced by the private sector would mirror those in the public sector, such as data availability, capacity building, and integration across systems. Recognising these hurdles, the Securities Commission Malaysia has adopted a phased and developmental approach to support companies in implementing NSRF. The first phase of reporting is for annual reporting periods on or after 1 January 2025, with full ecosystem-wide implementation, including assurance requirements, targeted for 2027.

To overcome data challenges, private entities are increasingly relying on digital tools and automation to collect, manage, and report sustainability data. This approach enhances efficiency and ensures accuracy, particularly in the context of complex disclosures. Additionally, training and capacity building are actively being addressed through programmes offered by MIA and other institutions. Companies are also engaging external consultants to bridge expertise gaps.

Another major hurdle is Scope 3 emissions reporting, which requires close collaboration with suppliers. In addition, many companies are implementing sustainable procurement practices by prioritising vendors with strong sustainability credentials.

Role of Public Sector Accountants

Datuk Nor Yati emphasised the importance of accountants developing the required skills to prepare for public sector sustainability reporting. To ensure success, Datuk Nor Yati Ahmad highlighted the importance of capacity building and training, recommending that accountants pursue professional development in the area of sustainability.

Datu Hajah Elean highlighted that accountants can help assess and prioritise sustainable investments, like renewable energy projects, by evaluating long-term costs and benefits. They also play a key role in incorporating sustainability goals into budgets, assisting in the creation of carbon budgets, and advising on securing green financing for renewable energy and sustainable forestry projects.

“Accountants can contribute by providing financial insights, risk management expertise, and promoting integrated decision-making that balances economic growth with environmental responsibility,” Datu Hajah Elean said.

In addition to financial management, accountants contribute to various sustainability initiatives, including analysing supply chain inefficiencies and supporting the transition to a circular economy. They ensure that sustainable projects are executed ethically and within financial frameworks, promoting transparency and trust. Datu Hajah Elean emphasised that accountants also play a central role in measuring the social impact of businesses, such as job creation and community development.

MIA Sustainability Blueprint and Roadmap

Puan Rasmimi explained that the MIA Sustainability Blueprint for the Accountancy Profession outlines sustainability aspirations and guiding principles, with a strong emphasis on the role accountants will play. She encouraged attendees to explore the Blueprint on the MIA’s website for further details.

To enable the Blueprint’s implementation, the MIA Council approved the MIA Sustainability Roadmap in January 2025, which encompasses 169 initiatives developed by sixteen MIA committees. These initiatives are structured around three main themes: capacity building, tools and guidance, and advocacy and collaboration. The MIA Public Sector Accounting Committee (PSAC), chaired by Datuk Nor Yati, is one of the key contributors to the roadmap, with several initiatives incorporated to support public sector accountants in their sustainability efforts. The Roadmap spans five years, aligning efforts across various sectors to drive the sustainability agenda forward.