By Roger Loh Kit Seng and Kwo Kah Men

The Debate on Valuation

Valuation is one of the most contested topics within the startup community. Founders often see it as a measure of progress. Investors treat it as a benchmark of performance. Regulators require it to be reported in a manner that allows for audit and comparison across companies.

The tension lies in the fact that a single company can be described with different valuations simultaneously, each serving a distinct purpose. A “headline valuation” figure quoted in a press release often tells a story that appears neat and appealing but hides the complexity of the layered financing terms. Accounting standards, on the other hand, require a different discipline: fair value measurement that reflects the actual economic position of various stakeholders.

This is not a debate confined to Silicon Valley or Bangalore. It is increasingly relevant in Malaysia, where the startup ecosystem has grown rapidly and where local investors, founders, and regulators are adapting to the complexities of capital structures.

Against this backdrop, MFRS 13 Fair Value Measurement serves as a standard that helps the ecosystem mature by providing a consistent language for interpreting and reporting value.

The Valuation Paradox in Practice

In June 2024, Malaysia-headquartered fintech Paywatch raised US$30 million through Series A equity and credit facilities, marking the largest funding round for an earned-wage access startup in Southeast Asia.¹ In August 2025, reports suggested that Singapore-based logistics unicorn Ninja Van was preparing an internal financing round at a valuation approximately 50% lower than its prior round.²

Both statements are factual, but they point in opposite directions: one firm is rising at record levels, while another is taking a hit on valuation. What they both reveal is that valuation is deal-specific. It depends on the class of shares issued, the rights attached to them, and the context of the transaction.

The most common measure quoted in the press, the headline valuation, is post-money valuation: the price per share in the latest round multiplied by the fully diluted share count. This measure assumes that all shares are identical in value. In reality, they are not. Preferred shares may have liquidation preferences, anti-dilution rights, or conversion options. Common shares do not. Options and convertible notes carry further complexity.

Why Malaysia Cannot Ignore the Issue

Malaysia’s startup ecosystem has gained real momentum. Seedtable reports that 23 notable startups have collectively raised about US$874 million, with an average of US$38 million per company.³ The Government has also played a role. Jelawang Capital’s Emerging Fund Managers’ Programme (EMP) and Regional Fund Managers’ Initiative (RMI) are part of a deliberate push to develop a more substantial venture capital (VC) landscape.⁴

This growth has led to more complex financing structures. Startups no longer stop at a single round of seed funding. They often go through multiple rounds, each with different classes of shares and rights attached to them. Without a proper framework, it isn’t easy to compare valuations across time or across companies.

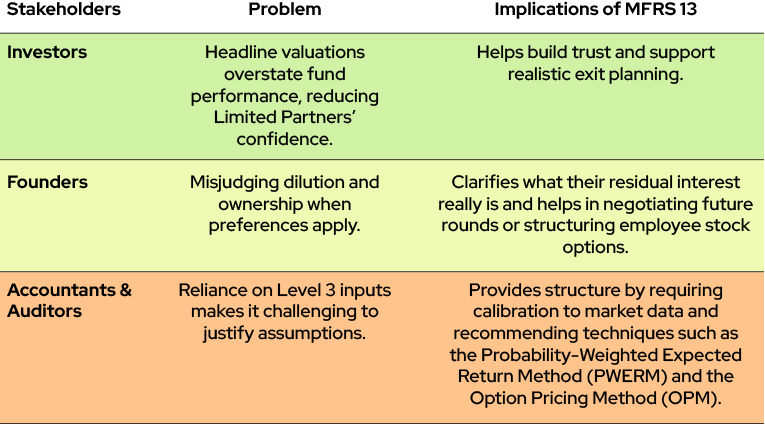

For investors, this raises the risk of overstating fund performance. For founders, it creates confusion about dilution and ownership. For auditors and regulators, it makes financial reporting harder to verify. MFRS 13 provides a framework that addresses all of these concerns.

A Practical Example: Startup ABC

Let us take a simplified case study.

Headline View

Startup ABC raises RM10 million for a 20% stake, implying a post-money valuation of RM50 million. A year later, the company sold for RM45 million. Looking only at the headline numbers, the outcome looks worse than expected: the exit value is lower than the earlier valuation.

Fair Value View

Now add a simple preference term. Investors hold non-participating preferred shares with a 1x liquidation preference. That means they must be paid back their RM10 million investment before common shareholders receive anything.

When the company is sold for RM45 million, the proceeds are distributed as follows:

The result is that common shareholders end up with RM35 million. This is far below the RM50 million implied in the headline post-money valuation.

This gap is not a rare occurrence. A US unicorn once reported a headline valuation of US$1 billion. A detailed analysis that accounted for liquidation preferences and other rights put the fair value closer to US$600–800 million.⁵

How MFRS 13 Bridges the Gap

MFRS 13 defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.⁶

The key points in that definition are:

- Price: Based on what a market transaction would produce, not internal estimates.

- Orderly transaction: Conducted under normal conditions, not a distressed or forced sale.

- Market participants: Independent and informed parties, such as venture capital funds, angel investors, corporate investors, or strategic acquirers.

By applying these principles, MFRS 13 compels stakeholders to look beyond the headline number and assess the securities’ actual market value.

Strategic Imperatives for Key Stakeholders

The Valuation Steps

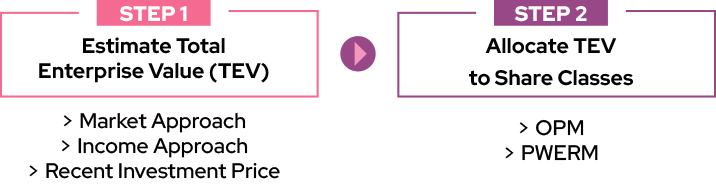

With the principles of MFRS 13 established, the next question is how valuers apply them in practice. Startup valuations typically rely on unobservable inputs (Level 3), given limited history, high uncertainty, and complex capital structures. The process usually involves two steps:

- Estimating TEV: Valuers typically consider a range of approaches, with the selection dependent on the startup’s stage and the quality of available market evidence.

- Market Approach: Using multiples from comparable companies or transaction deals. The challenges are that proper comparables are often scarce for early-stage firms.

- Income Approach: Discounted cash flow is more relevant for later-stage companies with clearer projections but highly speculative for pre-revenue startups.

- Recent Investment Price: A useful benchmark when third-party investors have participated. However, calibration must be applied and updated at each reporting date to reflect changes in the company’s or market conditions.⁷

- Allocating TEV (The “Waterfall”): The TEV is allocated to the various share classes according to their contractual rights.⁸ Common approaches include:

- OPM: Treats equity as a series of call options, modelling payout waterfalls dictated by liquidation preferences.⁹

- PWERM: Estimates value based on the probability-weighted outcomes of potential exit scenarios, beneficial when multiple strategic paths are under consideration.¹⁰

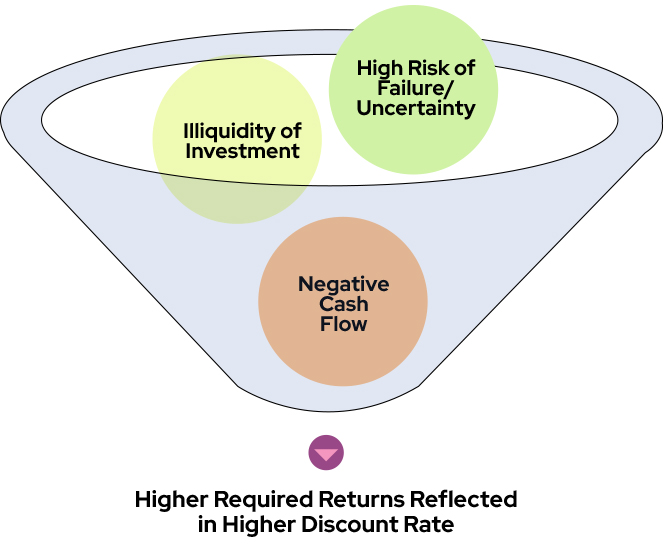

The Role of Discount Rate

The discount rate is a critical input that underpins both the Income Approach and the PWERM. Startups are risky and operate under far greater uncertainty than mature, listed companies with established performance records and liquid markets. In practice, this translates into higher discount rates in valuation models.

The risks include:

- High Risk of Failure and Uncertainty: Products are often unproven and face risks from development, regulation, and market acceptance. The high probability of failure requires a material risk premium.

- Illiquidity of Investment: Private company shares cannot be readily sold until an exit, such as an IPO or trade sale.

- Negative Cash Flow (“Cash Burn”): Startups typically incur heavy development expenditure with limited revenue. A short cash runway heightens the risk of distress and weakens negotiating power in future fundraising.¹¹

- High Required Rates of Return by Investors: Venture capital and private equity funds often target 25% or more returns to offset losses from failed investments. These return expectations are embedded in the higher discount rates applied in practice.¹²

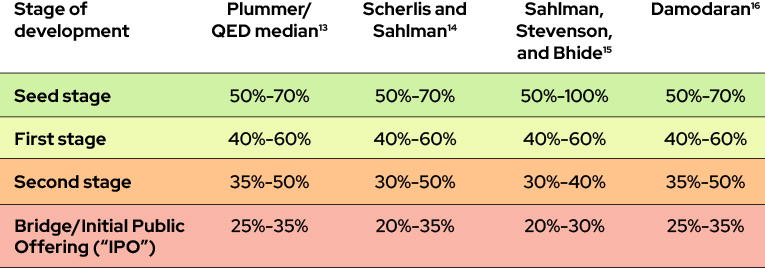

Empirical studies have documented discount rates ranging from 25% to 70%, depending on the stage of development. For example, seed-stage ventures are often modelled with discount rates of 50–70%:

Summing Up

Startups, by nature, thrive on ambition. They need compelling stories to attract talent, capital, and customers. Nevertheless, if those stories rest only on inflated headline valuations, the foundations become fragile. Investors lose confidence when reported numbers fail to align with actual outcomes. Employees, who often hold common shares or options, may find their expectations misaligned with reality. Founders risk misjudging dilutions, only to discover too late how much of their company has already been given away.

This is where MFRS 13 plays a deeper role. By insisting that valuations be anchored to fair value as defined by market participants, it forces all stakeholders to confront the true economics of a financing structure.

There is also a strategic dimension to this. Malaysia aspires to be a hub for innovation in Southeast Asia. To achieve this, it must attract not just local capital but also international investors who bring global networks and expertise. These investors expect standards that match those found in more mature markets. Adopting MFRS 13 signals that the ecosystem takes valuation seriously, and that the market can produce numbers investors can trust. Perhaps then, that is the real lesson. Valuation is not about chasing the largest number but ensuring that the number means something.

Note: The views reflected in this article are the views of the authors and do not necessarily reflect the views of Forvis Mazars or its member firms.

Roger Loh Kit Seng is a Director with Financial Advisory, Forvis Mazars in Malaysia and a member of the Valuation Committee of the Malaysian Institute of Accountants.

Kwo Kah Men is a Manager with Financial Advisory, Forvis Mazars in Malaysia.

¹ Digital News Asia. (2024, June 24). Malaysia-headquartered Paywatch secures US$30mil funding in largest raise for Earned Wage Access startup in SEA. Digital News Asia. https://www.digitalnewsasia.com/startups/malaysia-headquartered-paywatch-secures-us30mil-funding- largest-raise-earned-wage-access

² AsiaOne. (2025, August 13). Ninja Van cuts 12% of Singapore workforce after 2 rounds of layoffs in 2024. AsiaOne. https://www.asiaone.com/money/ninja-van-cuts-12-singapore-workforce-after-2-rounds- layoffs-2024

³ Seedtable. (2025, September 16). 23 Best Startups in Malaysia to Watch in 2025. Seedtable. https://www.seedtable.com/best-startups-in-malaysia

⁴ Digital News Asia. (2025, June 24). Jelawang Capital selects first round of EMP and RMI fund managers in boost to Malaysia’s VC ecosystem. Digital News Asia. https://www.digitalnewsasia.com/startups/jelawang-capital-selects-first-round-emp-and-rmi-fund- managers-boost-malaysias-vc-ecosystem

⁵ Harms, T.W. (2015, September 11). Unicorn Valuations: What’s Obvious Isn’t Real, and What’s Real Isn’t Obvious. Mercer Capital. https://mercercapital.com/unicorn-valuations-whats-obvious-isnt-real-and-whats-real-isnt-obvious/

⁶ Malaysian Accounting Standards Board. (2021). MFRS 13: Fair Value Measurement. MASB. https://www.masb.org.my/pdf.php?pdf=BV2021CR_MFRS13.pdf&file_path=pdf_file

⁷ Duff & Phelps, A Kroll Business. (2021, July). Valuation of early and growth stage technology companies. Malaysian Institute of Accountants (MIA).

⁸ Rane, A., & Shah, K. (2019, October 22). Business valuations using the Backsolve Method. Aranca.

⁹ Harms, T. W. (2016, May). A layperson’s guide to the option pricing model: Everything you wanted to know, but were afraid to ask. Mercer Capital.

¹⁰ International Institute of Business Valuers (iiBV). (2021). BV 204: Advanced topics in business valuation. Saudi Authority for Accredited Valuers (TAQEEM).

¹¹ Puca, A. (2020). Early stage valuation. Business Valuation Resources.

¹² London School of Economics and Political Science. Valuation: VC edition. London School of Economics and Political Science.

13 Plummer, J.L. (1989). QED Report on Venture Capital Financial Analysis. QED Research, Inc.

14 Scherlis D.R. and Sahlman W.A. (1998). A method for Valuing High-Risk, Long term, Investments: The Venture Capital Method. Havard Business School Note, 9-288-006. Havard Business School Publishing.

15 Sahlman W.A., Stevenson H., and Bhide A. (1998). Financing Entrepreneurial Ventures. Havard Business School Publishing.

16 Damodaran, A. (2009). Valuing young, start-up and growth companies: Estimation issues and valuation challenges. Stern School of Business, New York University.