By Thomas Chan Yeu Wai and Jane Wah Yu Zhen

Introduction

The Berry Ratio might sound like the latest fruit juice blend rather than a financial metric. Rest assured, it has nothing to do with berries or smoothies but certainly has to do with evaluating profitability in transfer pricing. This quirky sounding ratio plays a critical role in assessing arm’s length criteria, though its use as a Profit Level Indicator (PLI) often sparks transfer pricing disputes. In this article, we will peel back the layers and explore the nuances of the Berry Ratio, showing how it can be effectively applied in transfer pricing analysis—wherever it truly fits.

Background

The Berry Ratio is named after Dr Charles Berry, an American economics professor who introduced the concept during expert testimony in the 1979 transfer pricing litigation between DuPont and the United States tax authorities. In that case, Dr Berry analysed a distributor that also carried out marketing-related activities. He compared the ratio of gross profit to operating expenses of the tested entity against those of independent comparable companies. This approach enabled an assessment of whether the distributor earned an appropriate return on its value-adding activities, on the premise that the costs of those activities were reflected in its operating expense base.

The Berry Ratio measures the relationship between a company’s gross profit and its operating expenses.

Formula – Berry Ratio= Gross Margin / Operating Expenses

It is designed to assess whether an entity earns an arm’s length return relative to the operating costs incurred in performing its activities. In simple terms, a Berry Ratio >= 1 generally indicates that the entity is able to cover its operating expenses and earn a return, while a ratio < 1 suggests that operating costs are not fully recovered.

The Berry Ratio may be appropriate in circumstances where the tested party performs routine or support activities with limited value addition, does not own or exploit valuable intangibles, and does not assume economically significant risks such as inventory, market, or credit risks. In such cases, the returns earned by the entity are more closely linked to its operating effort (reflected in its operating expenses) than to sales.

Berry Ratio framework

Conceptually, the Berry Ratio looks like it is based on sound economic principles: a neat and tidy PLI that compares gross profit to operating expenses. It aligns well with the arm’s length principle, especially where value creation is tied more to operating costs than to assets or risks. But in practice, tax authorities don’t always sip the Berry Ratio as smoothly as its name suggests.

While the Berry Ratio is formally recognised by the Organisation for Economic Cooperation and Development (OECD) and adopted in many tax jurisdictions, including Malaysia, its practical application remains highly selective and is kind of served only on very selective menus.

Let us first understand the three formal conditions¹ relating to the appropriateness of the Berry Ratio, as laid out in the revised Malaysia Transfer Pricing Guidelines (MTPG) 2024, which are well aligned with the OECD framework.

Para 3.66

- The value of the functions performed is proportional to the operating expenses;

- The value of the function performed is not materially affected by the value of the products distributed, i.e., it is not proportional to the sales; and

- The taxpayer does not perform any other significant functions, such as marketing or manufacturing or any functions that add value to the products that should be remunerated using another method or financial indicator.

Our comments on criterion 1: The Berry Ratio hinges on operating expenses as its denominator, so it only works when value creation is tied directly to those costs. It means it is unsuitable in scenarios where other factors drive profitability such as transactions involving significant nonroutine intangibles, integrated distributors that also assemble or customise products, fullfledged distributors managing inventory and bearing related risks, or manufacturers whose cost base extends beyond operating expenses to include cost of goods sold.

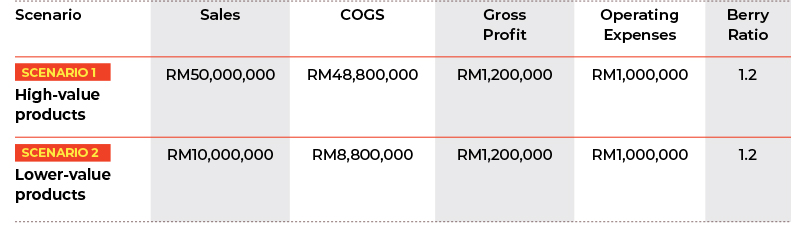

Our comments on criterion 2: This criterion can be demonstrated through the example below:

As evident from the above, even though sales values differ drastically (RM50 Mil vs RM10 Mil), the Berry Ratio remains the same (1.2) because the company’s value creation is tied to operating expenses, not to the sales value of the products.

Our comments on criterion 3: The Berry Ratio is appropriate only when the taxpayer performs routine functions. Where the entity undertakes significant activities—such as marketing, inventory, manufacturing, or other valueadding functions—profitability should instead be assessed using alternative methods or indicators. In practice, this third criterion is often a point of contention between tax authorities and taxpayers during audits.

- Further, MTPG 2024 also recognises the Berry Ratio’s relevance in intermediary arrangements –

- Para 3.67 – Berry Ratios can be useful in intermediary activities where taxpayers purchase goods from an associated person and on-sell them to another associated person. In this situation, the RPM may not be applicable due to the absence of uncontrolled sales, while the CPM may not be applicable due to controlled purchases. Operating expenses, however, may be reasonably independent from transfer pricing formulation. However, if the operating expenses have been materially affected by controlled transaction costs such as head office charges, rental fees or royalties paid to an associated person, the use of BR may not be appropriate.

- Our comments on Para 3.67:

Notably, the Inland Revenue Board of Malaysia (IRB) has revised its wording from “Berry Ratio is only useful” to “Berry Ratio can be useful” in the above paragraph compared to old Guidelines. This shift, though subtle, signals a meaningful change in approach. The earlier phrasing conveyed a restrictive stance. By contrast, the new phrasing introduces some flexibility.

Receptiveness during Tax Audits

The IRB increasingly challenges the use of the Berry Ratio during audits, particularly where the taxpayer’s functions have certain level of economic significance. As outlined in the three criteria above, the Berry Ratio is appropriate only when the taxpayer performs routine, lowrisk activities—without assuming inventory, credit, or market risks, and without owning or exploiting intangibles. In practice, this confines its application to lowrisk distributors engaged in basic administrative or facilitation roles, resembling service providers rather than true distributors such as Japanese general trading companies, commonly known as sogo-sosha companies. That said, situations are rarely black and white; hybrid cases often arise, making the analysis subjective and highly contextual.

When assessing the appropriateness of the Berry Ratio, the IRB typically focuses on the Malaysian entity’s role within the group supply chain and whether it undertakes valueadded activities. Such activities may include inventory management, holding key relationships with customers and suppliers, price negotiations, market development, credit management and other strategic decisionmaking matters. The taxpayer needs to establish that the entity merely acts as an information conduit—executing headquarters’ instructions without pricing authority and holding little or no inventory. Further, acceptance of the Berry Ratio by the IRB also depends heavily on whether the functional profile is consistently supported by contemporaneous documentation and evidence of actual conduct.

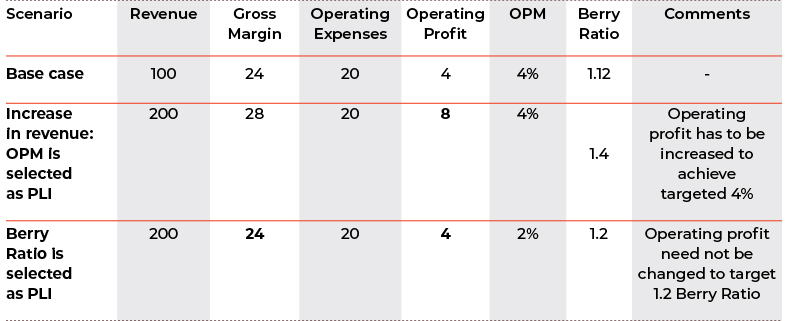

The IRB often considers Operating Profit Margin (OPM) as the PLI instead of Berry Ratio, since it generally produces higher profitability outcomes especially when revenue increases. This dynamic is illustrated below:

- Under OPM: Operating profit must increase to 8 to maintain 4% OPM. This would result in higher tax exposure, directly linking profitability to sales growth.

- Under Berry Ratio: The ratio is tied to operating expenses instead of revenue, therefore increase in revenue does not lead to an expectation of increase in profit to meet the arm’s length principle. Under the Berry Ratio, profit is expected to be increased only in case of increase in operating expenses. Therefore, this ratio is apt for entities with limited functionality, wherein expenses typically do not scale in proportion to sales, making Berry Ratio outcomes relatedly flat compared to OPM as PLI.

Key considerations in Applying the Berry Ratio

With rising challenges from the IRB in acceptance of Berry Ratio, taxpayers should carefully evaluate the following considerations before adopting the Berry Ratio as a PLI:

1. Accounting Disclosure

- Gross vs. Net Recording: Transactions recorded on a gross basis in financial statements are more likely to be challenged when the Berry Ratio is applied.

- Cost Classification Sensitivity: The Berry Ratio is highly sensitive to how costs are classified between operating expenses and cost of goods sold.

- Practical Implementation: Consistency is critical — the tested party’s Berry Ratio must be calculated in a manner congruent with that of the selected comparables.

2. Selection of Comparables

- Nature of Activities: Whether to benchmark against service providers or trading companies with routine functions is a key consideration.

- Disclosure Limitations: Publicly available data often lacks sufficient granularity, making careful selection of comparables essential.

- Empirical studies² show that wholesale distributors with low operating expense-to-sales ratios (10–15%) tend to report much higher Berry Ratios than those with higher expense-to-sales ratios. It implies that comparisons across companies with significantly different expense structures can distort outcomes.

3. Hybrid Cases

- Limited-Risk Activities: Taxpayers who perform activities such as inventory handling or attending customer/supplier meetings at the instruction of a counterparty — without bearing risk or exercising independent decision-making — face heightened challenges in defending Berry Ratio.

- Economic Significance: Where such activities have economic relevance to the overall business profile, authorities may argue that Berry Ratio does not adequately capture the tested party’s contribution.

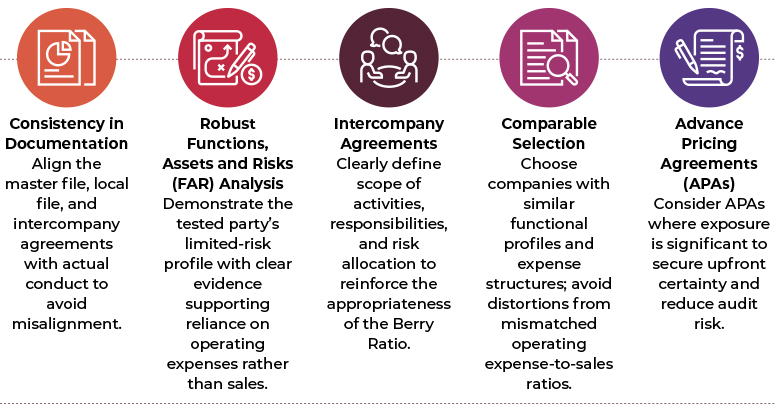

Key Safeguards for Defending the Berry Ratio

To effectively defend the use of the Berry Ratio as the selected PLI, taxpayers should adopt a structured, evidence-based approach, as follows:

Conclusion

The IRB’s increasing focus on PLI selection reflects a broader shift towards closer scrutiny of economic substance and value creation. And let’s be clear: the Berry Ratio is not a juice blend you sip at brunch — it’s a serious transfer pricing tool that only works in limited, well defined circumstances. Its application demands careful functional analysis, disciplined comparability assessment, and robust supporting evidence. Without these safeguards, taxpayers risk finding themselves in a sticky situation, facing heightened adjustments and disputes in Malaysia’s evolving audit landscape.

¹ Malaysia Transfer Pricing Guidelines 2024

² https://www.irs.gov/pub/irs-apa/apa_study_guide_.pdf

Thomas Chan Yeu Wai is Director, Tax-Transfer Pricing and Jane Wah Yu Zhen is Assistant Manager, Tax–Transfer Pricing of Deloitte Malaysia Tax Services Sdn. Bhd. (formerly known as Deloitte Tax Services Sdn Bhd)

The content in this article is the personal view of the authors and does not purport to reflect the views of Deloitte Malaysia.