By MIA Financial Statements Review Team

Borrowing costs play an important role in financial reporting, particularly for entities involved in significant construction activities or capital investment projects. Malaysian Financial Reporting Standard (MFRS) 123 Borrowing Costs sets out the requirements for the recognition, measurement, and disclosure of such costs.

Applying MFRS 123 correctly supports accurate financial reporting while enhancing transparency and alignment with regulatory expectations. By clearly defining when borrowing costs should be capitalised and how they should be accounted for, the standard enables entities to present a more faithful representation of their financial position and performance.

1. Objective of MFRS 123

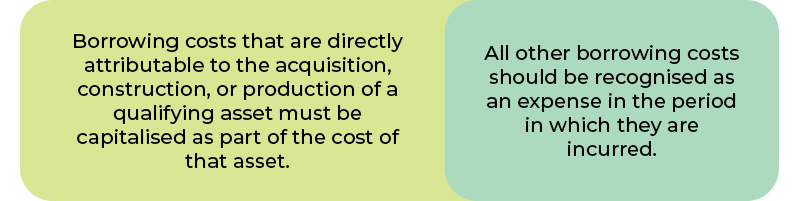

The primary objective of MFRS 123 is to prescribe the accounting treatment for borrowing costs. The standard mandates that:

This approach ensures that the cost of assets includes all necessary expenditures required to bring them to their intended use or sale condition, which gives a faithful representation of the cost of the asset and enhances comparability among all non-equity financed assets.

2. Scope of the Standard

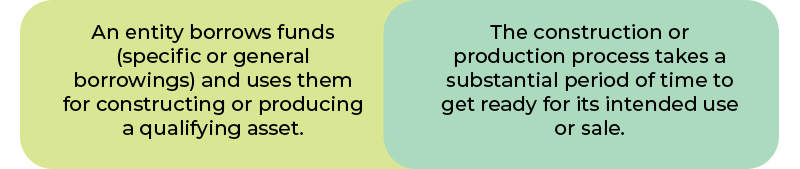

MFRS 123 applies to all borrowing costs. It applies specifically when:

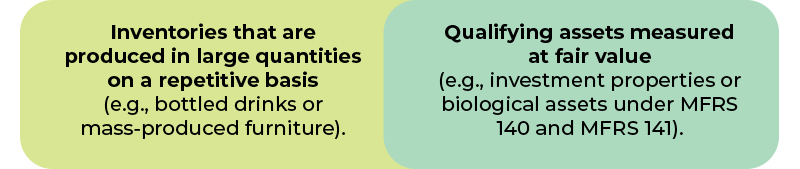

However, an entity is not required to apply the standard to borrowing costs related to:

3. Key Definitions

Understanding MFRS 123 begins with its fundamental definitions:

3.1 Borrowing Costs

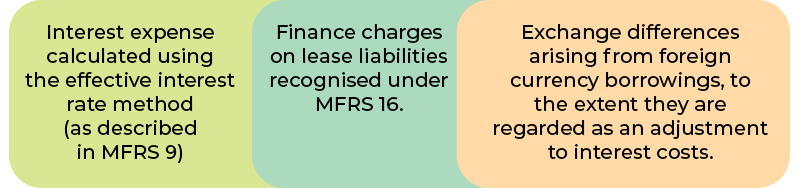

Borrowing costs include interest and other costs that an entity incurs in connection with borrowing funds. Examples include:

However, the periodic unwinding of the discount (i.e. accretion of interest) on obligations such as decommissioning, dismantling, or restoration obligations related to property, plant and equipment cannot be capitalised as part of the cost of the asset (see IFRIC 1.8).

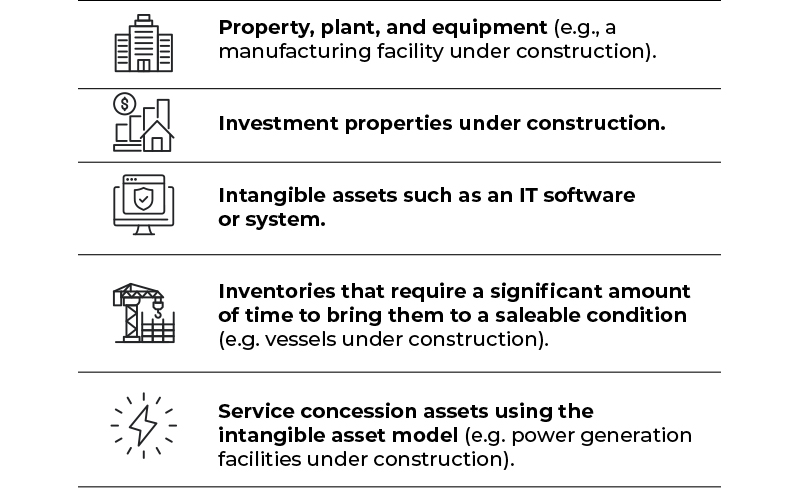

3.2 Qualifying Asset

A qualifying asset is an asset that necessarily takes a substantial period of time to get ready for its intended use or sale. These assets typically include:

4. Recognition Principles

4.1 Capitalisation of Borrowing Costs

An entity shall capitalise borrowing costs that are directly attributable to the acquisition, construction, or production of a qualifying asset as part of the cost of that asset.

Directly attributable borrowing costs are those that would have been avoided if the expenditure on the qualifying asset had not been made. This demonstrates a strong causal relationship between the borrowings and the creation of a qualifying asset.

4.2 Commencement of Capitalisation

Capitalisation of borrowing costs begins when all of the following conditions are met:

These conditions ensure that capitalisation begins only when activities necessary to prepare the qualifying asset for its intended use or sale have commenced (which encompass more than the physical construction of the asset), and not merely upon obtaining financing.

4.3 Suspension of Capitalisation

Capitalisation should be suspended during extended periods in which active development of the asset is interrupted. For example, if construction is halted for several months due to a strike, borrowing costs incurred during that period should be expensed.

Short or temporary delays, however, do not justify suspension. An entity does not suspend capitalising borrowing costs when a temporary delay is a necessary part of the process of getting an asset ready for its intended use or sale. For example, capitalisation continues during the extended period that high water levels delay construction of a bridge, if such high water levels are common during the construction period in the geographical region involved.

4.4 Cessation of Capitalisation

Capitalisation of borrowing costs must cease when:

In cases of development in stages, capitalisation ceases for each part that is substantially completed and ready for its intended use or sale.

5. Specific vs General Borrowings

Borrowings can be either specific (taken out for a particular qualifying asset) or general (funds borrowed for general purposes, and used for qualifying asset construction).

5.1 Specific Borrowings

When borrowings are made specifically for a qualifying asset, the actual borrowing costs incurred on that loan, less any investment income from the temporary investment of those borrowings, are to be capitalised.

For instance, if a company borrows funds specifically to finance the construction of a new factory, the interest on those borrowed funds (e.g. interest cost on bonds raised) is directly attributable and should be capitalised.

5.2 General Borrowings

When funds are borrowed generally and used for the purpose of obtaining aqualifying asset, the borrowing costs to be capitalised are calculated using a capitalisation rate determined using the weighted average of borrowing costs.

The amount of borrowing costs that an entity capitalises during a period shall not exceed the amount of borrowing costs it incurred during that period.

6. Group borrowings

When one group entity borrows funds to finance a capital project of another group entity, MFRS 123 requires capitalisation to be assessed based on which entity actually incurs the borrowing costs.

Hence, in the separate financial statements of the borrowing group entity, no capitalisation of interest is permitted as it does not have a qualifying asset. As for the group entity that constructs a qualifying asset, interest capitalisation is not permitted if it has not incurred an interest expense (e.g. interest free advances from the borrowing group entity).

However, in the consolidated financial statements, interest capitalisation is permitted as the group has a qualifying asset and a borrowing to fund the construction of the qualifying asset. Nevertheless, the amount of interest capitalised should reflect the interest cost to the group of borrowings from third parties which could have been avoided if the expenditure on the qualifying asset had not been made.

7. Disclosures

MFRS 123 requires the following disclosures:

These disclosures assist users of the financial statements in understanding the impact of capitalised borrowing costs on an asset’s value and overall financial performance, particularly concerning significant or long-term development projects.

Observations

This section aims to share the review findings of the Financial Statements Review Committee (FSRC or the Committee) relating to disclosures made in the financial statements and their accompanying notes to the financial statements. However, it does not delve into matters related to determining the recognition and measurement of borrowing costs.

Comments discussed herein are intended to be applied within the context of the specific facts and circumstances associated with the identified observations. It is not intended to be exhaustive and does not address all potential issues relating to borrowing costs.

In addition, careful consideration and judgement should be applied in each individual fact and circumstance since Malaysian Financial Reporting Standards (MFRS) are principles-based.

Review findings

Below are the observations noted by the FSRC relating to the disclosures of borrowing costs of public-listed companies/entities (PLCs).

Observation 1

There were significant additions to capital work-in-progress (CWIP) during the financial year.

It was enquired:

- Whether the CWIP meets the definition of a qualifying asset;

- What is the source of funding for the CWIP;

- Whether any borrowing costs incurred that should be capitalised in accordance with MFRS 123; and

- If yes, please provide the relevant disclosures in accordance with the requirement of Paragraph 26(a) and (b) of MFRS 123.

Response from PLC

The capital work-in-progress (CWIP) comprises buildings under construction and machinery under installation, both of which require a substantial period of time to be ready for their intended use. Accordingly, the CWIP meets the definition of a qualifying asset.

The CWIP was financed entirely through loans from related companies. As the CWIP was fully funded from internal sources, no borrowing costs were capitalised in accordance with MFRS 123.

The group’s bank borrowings were mainly utilised for trade and working capital purposes, as well as for the settlement of bank and other loans, and were not attributable to the CWIP.

Accordingly, there was no capitalisation of borrowing costs.

Observation 2

There were CWIP presented for more than one reporting period. However, it was noted that there were no disclosures on borrowing cost capitalised and the related capitalisation rate used.

Response from PLC

No borrowing costs were capitalised for the CWIP, as the project was funded from internally generated funds. Additionally, the bank borrowings were primarily utilised for trade activities, working capital needs, and the settlement of existing bank and other loans.

As the borrowings were not directly attributable to the acquisition, construction, or production of the CWIP, the capitalisation disclosure requirements under MFRS 123 are not applicable.

FSRC’s comments on Observation 1 and Observation 2

Paragraph 14 of MFRS 123 states that to the extent that an entity borrows funds generally and uses them for the purpose of obtaining a qualifying asset, the entity shall determine the amount of borrowing costs eligible for capitalisation by applying a capitalisation rate to the expenditures on that asset. The capitalisation rate shall be the weighted average of the borrowing costs applicable to all borrowings of the entity that are outstanding during the period. However, an entity shall exclude from this calculation borrowing costs applicable to borrowings made specifically for the purpose of obtaining a qualifying asset until substantially all the activities necessary to prepare that asset for its intended use or sale are complete. The amount of borrowing costs that an entity capitalises during a period shall not exceed the amount of borrowing costs it incurred during that period.

Such borrowing costs are considered as directly attributable to the qualifying asset even if the funds are borrowed generally as the borrowing costs would have been avoided if the expenditure on the qualifying asset had not been made (for example the entity could have repaid the general borrowings if it did not need to incur costs and cash flows to construct the qualifying asset).

Further, Paragraph 15 of MFRS 123 states that in some circumstances, it is appropriate to include all borrowings of the parent and its subsidiaries when computing a weighted average of the borrowing costs; in other circumstances, it is appropriate for each subsidiary to use a weighted average of the borrowing costs applicable to its own borrowings.

The PLC should evaluate if the conditions in Paragraph 17 of MFRS 123 are met and carefully determine whether the transactions fall within the scope of MFRS 123. If these conditions are met, the borrowing cost should be capitalised and related disclosure requirements would need to be complied with.

Conclusion

MFRS 123 provides a clear, principle-based framework for the accounting treatment of borrowing costs. By requiring the capitalisation of borrowing costs that are directly attributable to qualifying assets, the standard gives a faithful representation of the cost of the asset and comparability among all non-equity financed assets presented in the financial statements.

Effective application of MFRS 123 involves the exercise of professional judgement, supported by consistent practices and comprehensive documentation. Whether applied to major construction projects or other qualifying asset developments, the standard ensures that the financial impact of borrowing activities is appropriately reflected in the financial statements.

In addition, proper disclosure of borrowing costs further enhances transparency surrounding an entity’s financing arrangements and asset development processes. This level of transparency contributes to greater confidence in the financial statements among investors, regulators, and other stakeholders.