By the MIA Sustainability, Digital Economy and Services Team

As the climate change agenda gains momentum globally, stakeholders expect organisations to disclose their climate governance and impacts transparently. Public sector organisations are no exception, and the burden of disclosure is arguably heavier given their accountability to the public.

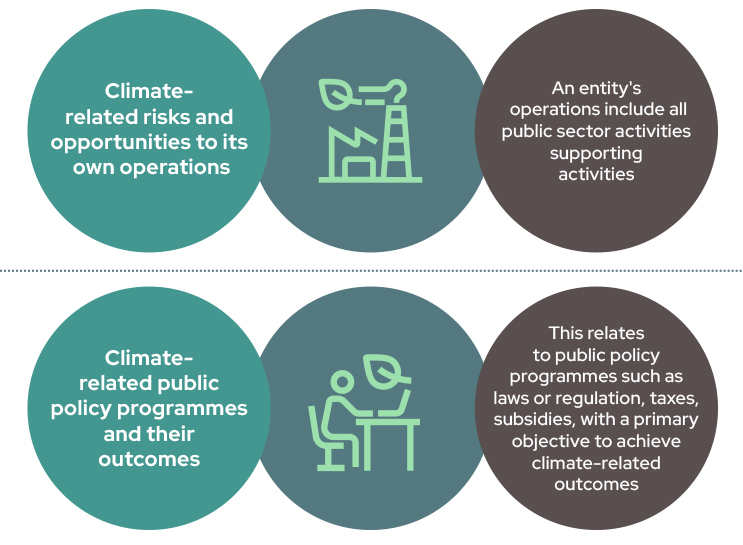

In January 2026, the International Public Sector Accounting Standards Board (IPSASB) issued its inaugural Sustainability Reporting Standard, IPSASB SRS 1 Climate-related Disclosures, to support public sector agencies and governments in adopting sustainability reporting, IPSASB SRS 1 will be adopted in two phases. Phase 1 focuses on climate-related disclosures for an entity’s own operations, while Phase 2 will address disclosures related to public policy programmes, recognising the unique role of governments.

For Phase 1, IPSASB issued IPSASB SRS 1 Climate-related Disclosures on 29 January 2026, marking a major milestone in establishing a global sustainability reporting standard for the public sector. The standard provides a globally consistent framework for public sector entities to disclose climate-related risks and opportunities, covering governance, strategy, risk management, and metrics and targets, with alignment to the IFRS S2 Climate-related Disclosures. Phase 1 will be effective from 1 January 2028, earlier adoption is permitted.

While for Phase 2, IPSASB will develop a separate standard for those specific public sector entities responsible for climate-related public policy programmes and their outcomes by December 2026.

Reframing Climate Disclosures: IPSASB’s Roadmap to Sustainable Public Sector Reporting

Prior to the issuance of SRS 1, this landmark development (at the ED or exposure draft stage) and its implications were discussed during the session on “Reframing Climate Disclosures: IPSASB’s Roadmap to Sustainable Public Sector Reporting” at the MIA International Accountants Conference 2025 in June 2025. Expert speakers Dr Nurmazilah Mahzan, Member of the MIA Sustainability Committee and the IFRS Integrated Reporting and Connectivity Council; Phang Oy Cheng, Executive Director, Head of Sustainability Advisory in KPMG Malaysia; and Henning Diederichs, Public Sector Sustainability Reporting Specialist at the Institute of Chartered Accountants in England and Wales (ICAEW) shared their insights on IPSASB’s efforts, moderated by Siti Farhana Sheikh Yahya from Astro Awani.

What is IPSASB SRS™ ED 1?

At the time of the conference, IPSASB was actively deliberating the responses received on its IPSASB Sustainability Reporting Standards Exposure Draft 1, Climate-related Disclosures (IPSASB SRS ED 1).The session therefore centred on IPSASB SRS ED 1, enabling delegates to better understand the proposals under consideration and the direction for public sector sustainability reporting.

A defining feature of IPSASB SRS ED 1 is its alignment with the IFRS Sustainability Disclosure Standards, enabling comparability between public and private sector sustainability reporting. For Malaysia, this alignment is timely with the country’s 2050 net-zero emissions goal, commitment to the Paris Agreement, and participation in the UN Sustainable Development Goals (SDGs) which demands an integrated approach across sectors.

The objective of this ED is to provide principles for public sector entities to disclose information in its general-purpose financial reports about¹:

Aligned with the Task Force for Climate-related Disclosures (TCFD) and IFRS S2 Climate-related Disclosures, IPSASB SRS ED 1 requires public sector entities to disclose:

Putting Public Sector Accountants at the Core of Climate Action

Accordingly, the standard will have several positive impacts on climate governance and accountability internationally and locally and in turn, the role of accountants.

Importantly, IPSASB SRS ED 1 aims to ensure comparability across jurisdictions while allowing sufficient flexibility for local adaptation, stated Henning Diederichs.

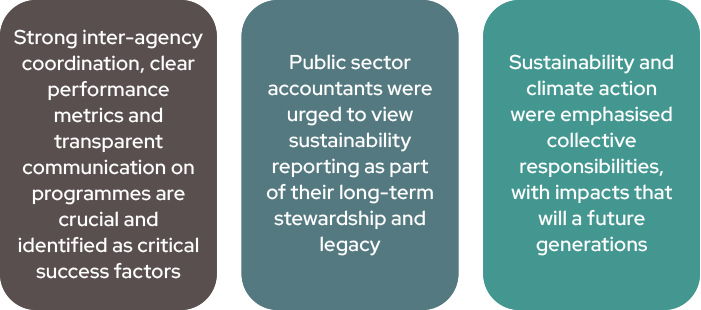

Phang Oy Cheng noted that this pronouncement allows public sector accountants to support coherent national climate action, as they are central to establishing data systems, embedding climate risk into budgets and performance frameworks, and ensuring that disclosures are credible and verifiable.

Reminding delegates that Malaysia has pledged to reduce carbon intensity relative to GDP by 45% by 2030² and is introducing policies such as the Energy Efficiency and Conservation Act (EECA) 2024, Dr. Nurmazilah said that ministries must therefore adopt unified sustainability frameworks to track data and monitor progress. She underscored that Malaysian public sector accountants are uniquely positioned to lead this transition due to their dual mandate of financial stewardship and public accountability.

From Policy to Practice: The Road Ahead

Translating standards into action will not be without challenges. The panellists collectively identified several obstacles to implementation, and recommended strategies to address these:

- Data Availability and Quality

Data is a key challenge, and many agencies lack systems to capture reliable emissions and climate risk data. Dr. Nurmazilah encouraged accountants to start small—track energy and water use, categorise sustainability-related expenditures, and progressively refine the data being collected. - Capacity and Skills

Specialised expertise in climate risk assessment, scenario analysis, and sustainability assurance remains scarce. Henning recommended that public sector accountants harness their acumen and upskill to be able to interpret complex climate data for decision-makers in the public sector, supporting informed decision-making for good governance. - Inter-Agency Coordination

Silos in the public sector can hamper inter-agency coordination. Effective reporting requires strong cross-government collaboration, which is often difficult to achieve due to differing mandates, priorities and data systems across agencies. “We need to move in the same direction,” Henning stressed. Dr. Nurmazilah proposed that the Accountant-General’s Department of Malaysia (AGD) could play a coordinating role by leveraging its strength in managing financial data. - Mindset Shift

An entrenched public sector mindset remains a significant barrier to effective sustainability reporting. Shifting mindsets and culture requires time, persistence, and leadership. Dr. Nurmazilah called on accountants to “make it our call and our purpose,” emphasising that even small steps can lead to systemic change. - Financing and Resource Allocation

Sustainability initiatives often require significant financial investment, yet dedicated funding and clear financing mechanisms are frequently lacking. Oy Cheng pointed out that sustainability initiatives are rarely cheap, and must be facilitated by strategic budgeting and financing mechanisms.

Measuring What Matters: From Numbers to Narratives

How should public sector entities get started on the climate disclosure journey?

While data and quantitative indicators are critical, Henning advised that governments should initially focus on qualitative disclosures, articulating how climate policies affect organisational outcomes and societal well-being.

Governments should also be mindful of challenges arising from reconciling short-term governance terms with long-term climate ambitions, he said. He noted that a key challenge faced by the UK under the Task Force on Climate-Related Financial Disclosures (TCFD) framework, related to inconsistent time horizons across political and climate cycles which complicated implementation.

Organisations can also use integrated thinking as a starting point. Dr. Nurmazilah emphasised the integrated nature of sustainability, which extends beyond numbers and connects financial and non-financial impacts. “Our role as accountants is to connect both worlds,” she said. For instance, link the utility bills paid by organisations back to the metric tonnes equivalent of carbon emissions generated to calculate their impact. Earlier in the session, she had also noted that a number of public sector agencies have already embarked on integrated reporting which incorporates non-financial disclosures. For instance, the Sustainable Energy Development Authority (SEDA) has highlighted its renewable energy and decarbonisation initiatives in its annual report, while the Accountant General’s Department of Malaysia has initiated training programmes to kick-start integrated and sustainability reporting within the public sector.

Through integrated thinking, organisations can better measure emissions, and in the bigger picture, assess the effectiveness of public policy programmes and the efficiency of resource allocation.

Leadership, Collaboration, and Purpose

Collectively, the panellists called for action at every level. In particular, public sector accountants are urged to play a central role in anchoring sustainability reporting and disclosures for better accountability and governance.

¹ IPSASB, October 2024, IPSASB SRS ED 1 – Climate-related Disclosures,

https://www.ipsasb.org/publications/ipsasb-srs-exposure-draft-1-climate-related-disclosures

² Ministry of Economy, 29 August 2023, National Energy Transition Roadmap,

https://ekonomi.gov.my/sites/default/files/2023-09/National%20Energy%20Transition%20Roadmap_0.pdf