By MIA Surveillance and Enforcement

Background and Context

Where an audit firm has been assigned a Type 3 rating under the Malaysian Institute of Accountants (MIA) Practice Review Programme, the Practice Review Committee (PRC) may, at its discretion, issue one of the following orders to facilitate remediation and enhancement of audit quality:

Order 3A – Peer Review Requirement

The firm shall be required to engage an independent peer reviewer to perform a structured review of its audit quality over a twenty-four (24)-month monitoring and remediation period, subject to PRC oversight.

Order 3B – Quality Assessment Programme (QAP)

The firm shall be required to undergo a structured Quality Assessment Programme (QAP) administered jointly by MIA and MICPA.

Following PRC’s approval of the proposed peer reviewer for an Order 3A, the 24-month monitoring and remediation process will commence. This process is considered final once initiated. Therefore, the selection and nomination of the peer reviewer should be undertaken with due care, objectivity, and professional judgement to support a consistent and effective remediation process.

For details on the peer reviewer approval process for Type 3 (Order 3A), please refer to https://www.at-mia.my/2025/06/10/the-peer-reviewer-approval-process-for-type-3-order-3a-audit-firms-a-critical-step-in-effective-remediation/

Subsequent Change of Peer Reviewer

Once the peer reviewer has been approved and the 24-month monitoring and remediation process has commenced, any subsequent change of the approved peer reviewer shall be strongly discouraged and will only be considered under exceptional and justifiable circumstances.

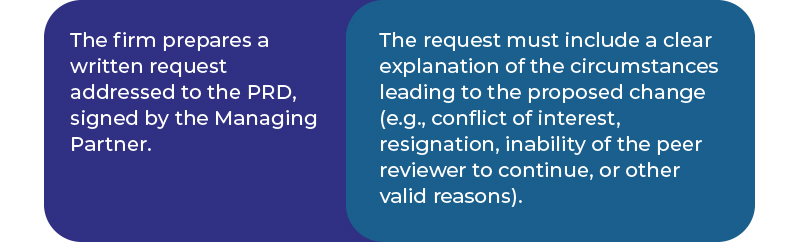

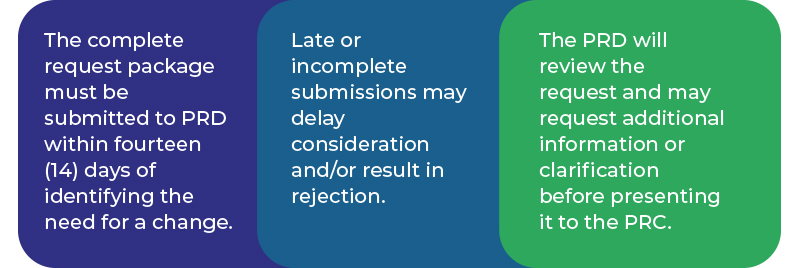

A firm seeking to replace its approved peer reviewer must submit a written request to the Practice Review Department (PRD), clearly outlining the reasons for the proposed change and including supporting documentation. The PRD will review the submission and determine whether the request is substantiated and reasonable, and the matter will then be tabled for PRC’s consideration.

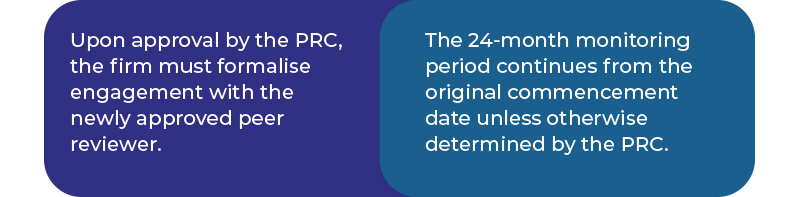

Approval for any change is at the sole discretion of the PRC. Firms should note that an approved change does not automatically reset or extend the 24-month monitoring period unless specifically determined by the PRC.

Firms are reminded to exercise due care and diligence in the initial selection process of a peer reviewer to ensure that the individual possesses the necessary competence, independence and capacity to complete the full duration of the monitoring period.

Any change should only be considered as a last resort and undertaken only when continuing with the existing reviewer is no longer feasible or appropriate.

Exceptional and Justifiable Circumstances for Changes

Requests for a change of peer reviewer may be considered only under the following situations:

- Resignation, unavailability, or incapacity of the existing peer reviewer.

- Conflict of interest or independence issue identified after approval.

- Significant deterioration in performance or conduct that may compromise the integrity of the monitoring process.

- Other exceptional and well-justified circumstances as accepted by the PRC.

Procedures for Requesting a Change of Peer Reviewer

Preparation of Request

Supporting Documentation

The request must be accompanied by the following documents:

- Written communication or evidence supporting the reason for the change (e.g., resignation letter, correspondence, or other relevant documents).

- Details of the proposed new peer reviewer, including a declaration of good standing and confirmation by the audit firm as part of the application process for PRC’s approval. This declaration confirms that the proposed peer reviewer meets the required qualifications and maintains good standing with MIA.

- A duly signed consent form from the proposed peer reviewer, confirming his/her agreement to serve in this capacity, eligibility, and commitment to comply at all times with the requirements, obligations, and professional standards prescribed by MIA, including those applicable to the conduct of peer review engagements.

- A transition plan, outlining how the change will be managed to ensure continuity of the monitoring and remediation process.

Submission to PRD

PRC Review and Approval

- The request will be tabled for PRC’s consideration, and the firm will be notified of the decision in writing.

Implementation

For more information on the role of the peer reviewer in the 24-month remediation process, please refer to https://www.at-mia.my/2025/06/10/the-peer-reviewer-approval-process-for-type-3-order-3a-audit-firms-a-critical-step-in-effective-remediation/

Reporting Obligation

While the appointed peer reviewer has no direct reporting obligation to the PRC, they are required to submit a completion report to the PRC confirming that the rectification process has been completed.

With respect to the audit firm, it should be noted that the firm remains fully responsible for providing timely updates on its rectification and remediation progress. The firm is required to submit its first annual progress update to the PRC no later than twelve (12) months from the PRC’s approval of the initial peer reviewer. Failure to submit the required progress update within the stipulated timeframe may constitute non-compliance with the monitoring and remediation requirements under Order 3A.

Conclusion

The careful appointment of a peer reviewer and adherence to the PRC monitoring and remediation requirements are critical for maintaining and improving audit quality among Type 3 firms.

Firms are therefore urged to exercise careful judgement and due diligence during the initial selection of the peer reviewer and to maintain open, transparent communication with the PRC throughout the process. Any request for a subsequent change should be made only when absolutely necessary, supported by valid justification and documentation.

A request for a subsequent change of peer reviewer is not only a tedious and time-consuming process, but more importantly, it may disrupt the rectification and monitoring progress of the audit firm. Such changes may also lead to inconsistencies or confusion if the outgoing and incoming peer reviewers adopt different approaches or methodologies in guiding the firm’s remediation efforts. This may compromise the effectiveness and timeliness of the entire rectification process. By exercising due diligence in the initial appointment and minimising unnecessary changes thereafter, firms contribute meaningfully to the broader goal of upholding audit quality, professional integrity and public trust.

PRC’s oversight is intended to ensure compliance, support continuous improvement, and promote sustainable audit quality in the profession.

Insights gathered from a poll held during a recent webinar session on 12 March 2026, “Understanding Peer Review Criteria under MIA’s Practice Review Framework” provide additional perspectives on the practical considerations faced by practitioners through a series of poll questions.

Note: The peer reviewer approval process for Type 3 (Order 3A), as outlined in the article published on 10 June 2025 titled “The Peer Reviewer Approval Process for Type 3 (Order 3A) Audit Firms: A Critical Step in Effective Remediation”, remains applicable and has not been superseded by the poll conducted during the webinar session held on 12 March 2026, “Understanding Peer Review Criteria under MIA’s Practice Review Framework”.

Refer to the following page for a summary of the poll questions, responses and key findings

Disclaimer – This article is intended to provide general procedural guidance and does not replace or override any applicable laws, regulations, or decisions of the Practice Review Committee, which retains full discretion in all matters.

Member Poll Insights: Peer Reviewer Readiness and Challenges

The following takeaways are based on responses from the webinar “Understanding Peer Review Criteria under MIA’s Practice Review Framework”

Overview

A total of 107 members participated in the poll, providing valuable insights into their readiness to undertake the role of Peer Reviewer, as well as the challenges and support required.

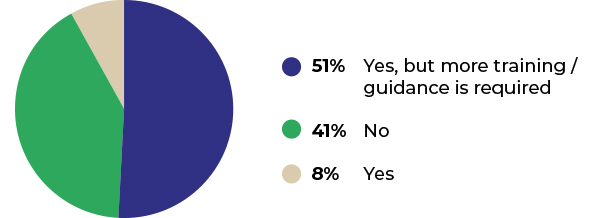

Q1: Willingness to be Appointed as a Peer Reviewer

“After learning the role and scope of a Peer Reviewer for Type 3 firms, would you be willing to be appointed?”

Key Insight: While there is moderate interest, the majority of respondents indicated a need for additional training and guidance, highlighting a capability gap rather than a lack of willingness.

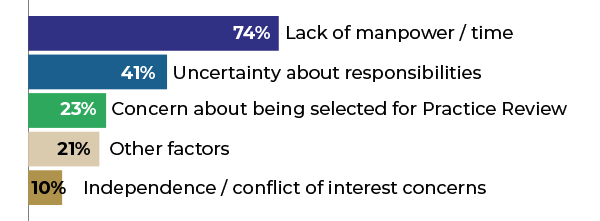

Q2: Key Challenges in Accepting the Role (Multiple responses allowed)

“What challenges might discourage you from accepting a Peer Reviewer role?”

Key Insight: The most significant barrier is resource constraints (time and manpower), followed by unclear expectations of the role, suggesting the need for clearer communication and practical support.

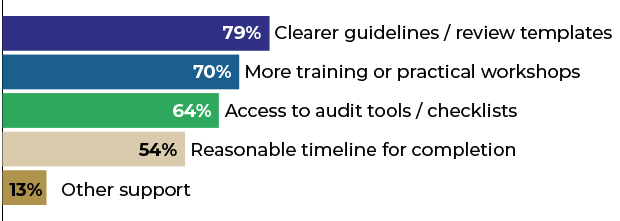

Q3: Support Needed to Encourage Participation (Multiple responses allowed)

“What support would encourage you to take up the role?”

Key Insight: Respondents emphasised the importance of structured guidance and practical tools, alongside capacity-building initiatives, to build confidence and encourage participation.

Overall Takeaways – There is clear willingness among members to undertake the role of Peer Reviewer. However, participation is primarily constrained by capacity limitations and a lack of clarity regarding expectations, rather than any inherent reluctance. Accordingly, targeted interventions, such as enhanced training and well-defined guidelines, would play a significant role in strengthening confidence and increasing participation rates.

In this regard, MIA PRD will continue to provide appropriate and sufficient guidance to support members and encourage greater participation in the Peer Reviewer programme. This initiative contributes to the profession by supporting fellow practitioners while offering valuable opportunities for peer reviewers themselves to enhance their own competencies and improve audit quality.