By MIA Sustainability, Digital Economy and Services team

Climate change is increasingly recognised as a pressing fiscal and governance challenge that demands immediate and coordinated action. Public sector accountants can play a central role in strengthening governance, enhancing sustainability reporting, and supporting climate-resilient public finance.

MIA recently hosted a complimentary webinar titled “The Role of Public Sector Accountants in Driving Climate Resilience”, bringing together global and local perspectives on the matter. Moderated by Rasmimi Ramli, Executive Director of Sustainability, Digital Economy and Services, the webinar featured Angela Ryan, Member of the International Public Sector Accounting Standards Board (IPSASB), Farhana Jabir, Director of Sustainability and Climate Change at PwC Malaysia.

Climate Change: A Fiscal and Governance Imperative

Rasmimi emphasised the urgency of climate action, citing episodes of extreme heat in Malaysia that necessitate cloud-seeding operations, as well as legal actions by Malaysian youth advocating for forest conservation. These developments illustrate the tangible and societal impacts of climate change. Globally, the World Meteorological Organisation has confirmed that the past decade was the hottest on record, with extreme weather events causing significant economic and social disruptions.¹

“As we look at recent developments, the data has really given us the urgency of looking at climate and the actions that we need to take,” she remarked.

Rasmimi also highlighted broader societal and legal developments, including initiatives to safeguard Malaysia’s forest and the anticipated introduction of a carbon tax framework. These developments reinforce the notion that climate change is not merely an environmental issue but a core public sector finance concern with significant implications for governance, policy, and resource allocation.

Why Climate Resilience Is Central to Public Sector Finance

Angela explained that climate resilience refers to an entity’s ability to adapt to both physical risks, such as floods and heatwaves, and transition risks arising from policy and technological shifts toward a low-emissions economy.

“When you look at that broad understanding of what climate resilience is, it seems almost very obvious that it’s a public sector finance issue,” she said.

Angela further noted that Governments often act as the “insurer of last resort,” bearing the responsibility of supporting communities in the aftermath of climate-related disasters. This expectation places significant pressure on public finances and underscores the importance of integrating climate considerations into fiscal planning.

Advancing Sustainability Reporting: The Role of IPSASB

Angela highlighted the issuance of IPSASB Sustainability Reporting Standard (SRS) 1 Climate-related Disclosures.

“The IPSASB made the decision that the first sustainability project would be climate-related disclosures,” she explained, noting that the standard is closely aligned with IFRS S2 Climate-related Disclosures to promote global consistency.

Angela described IPSASB’s two-phased approach in relation to climate-related disclosures, which distinguishes between disclosures related to an entity’s own operations and those concerning the public policy role of Governments. This distinction recognises the unique responsibilities of public sector entities as both service providers and policymakers.

Readiness for Climate and Sustainability Reporting

Farhana observed that public sector entities are at varying stages of readiness in adopting sustainability reporting. While federal and state Governments form the core of the public sector, statutory bodies, Government-linked companies (GLCs), and Government-linked investment companies (GLICs) also play significant roles.

“We do see quite a few of them actually have started to prepare sustainability reporting because they are providing critical services and understanding how this impacts their stakeholders is important.”

However, Farhana also highlighted the challenges posed by fragmented climate-related data across different ministries and agencies, as well as the limited public disclosure of the impact of climate change on Government operations.

A notable example is Bank Negara Malaysia, whose reporting distinguishes between its operational emissions and its policy influence on the financial sector. This dual approach aligns closely with the IPSASB’s approach as shared by Angela and provides a valuable model for other public sector entities.

Global Lessons: Insights from New Zealand and Beyond

Angela shared insights from New Zealand’s experience, emphasising the country’s strong foundation in accrual accounting and its evolving journey toward climate-related reporting.

Mandatory Climate Reporting Framework

One of the key developments highlighted by Angela is New Zealand’s mandatory climate-related disclosure regime, introduced by the External Reporting Board (XRB). XRB is an independent Crown entity, that is responsible for financial reporting, climate reporting, auditing and assurance and professional and ethical standards in New Zealand.² Although primarily targeted at private sector entities, particularly those participating in capital markets, Aotearoa New Zealand Climate Standards establish a useful benchmark and encourage voluntary adoption by other Government agencies seeking to enhance their sustainability reporting practices.

The standards are closely aligned with the Task Force on Climate-related Financial Disclosures (TCFD) and the IFRS Sustainability Disclosure Standards (IFRS S1 and S2). Importantly, certain public sector entities such as local Governments or agencies that issue debt securities are also required to comply. For example, the Auckland Council, which raises funds through international capital markets, is subject to these mandatory disclosure requirements. This demonstrates how market participation can act as a catalyst for enhanced transparency and accountability within the public sector.

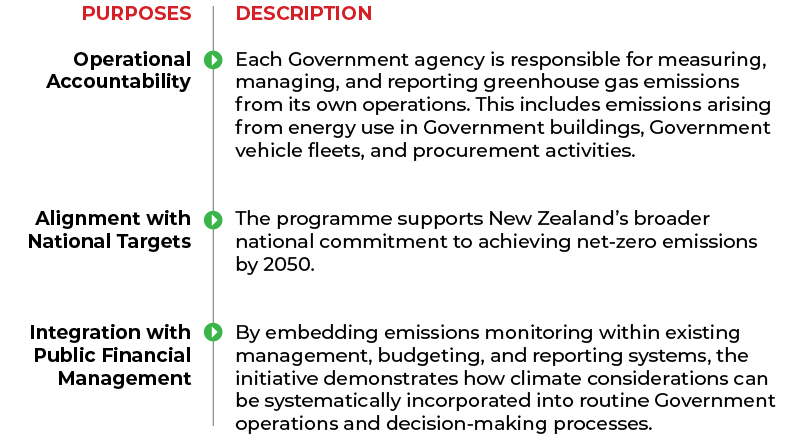

The Carbon Neutral Government Programme

Another significant initiative is New Zealand’s Carbon Neutral Government Programme (CNGP). This programme requires central Government agencies to measure, manage, and reduce their greenhouse gas emissions, focusing primarily on Scope 1 and Scope 2 emissions, with gradual inclusion of Scope 3 emissions where feasible.

The programme serves several important purposes as follows³:

Lessons from Leading Jurisdictions

Angela also highlighted exemplary practices from other jurisdictions that offer valuable insights for Governments worldwide.

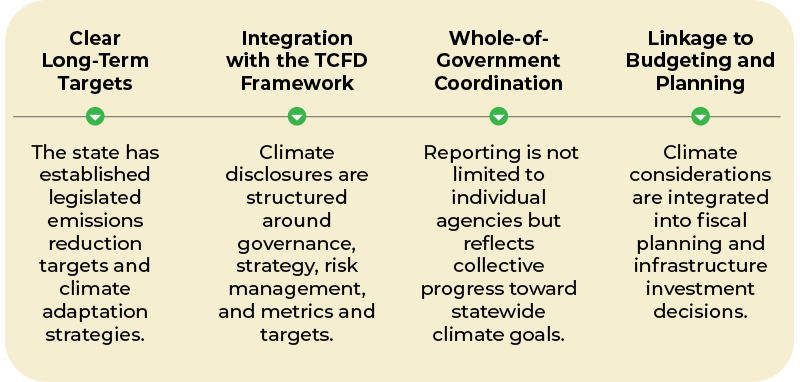

State of Victoria, Australia

The State of Victoria is recognised as a leader in public sector climate reporting. Its approach is characterised by a top-down, whole-of-Government strategy, where climate commitments are embedded within legislation and long-term policy frameworks.

Key features of Victoria’s approach include:

This comprehensive and coordinated approach enhances transparency and enables citizens to track the Government’s progress toward achieving its climate objectives.

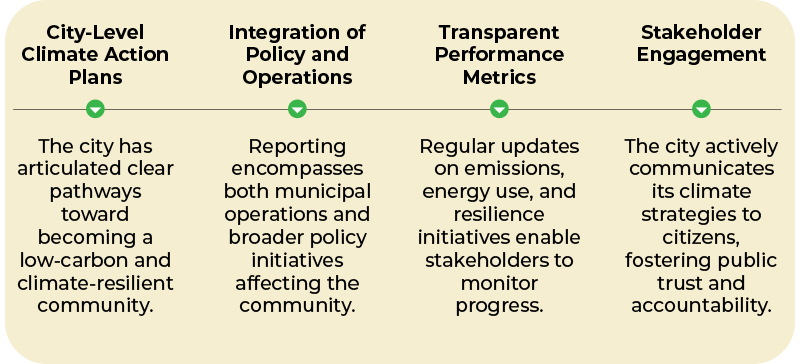

City of Vancouver, Canada

Angela shared that the City of Vancouver is a good example of how local Governments can lead in climate-related disclosures.

Key elements of Vancouver’s leadership include:

These initiatives demonstrate how municipalities can play a pivotal role in advancing climate action and serve as practical models for other jurisdictions.

Integrating Climate Considerations into Public Financial Management

Farhana explained that while climate data is increasingly used to inform policy decisions, integrating it into day-to-day operational decision-making remains a challenge.

This shift requires development of new metrics and analytical frameworks, such as greenhouse gas emissions and broader socio-economic impacts, to complement traditional financial indicators.

Angela further emphasised the importance of building a reliable climate and sustainability data ecosystem. She recommended starting with an inventory of existing datasets and focusing on information that supports risk management and decision-making.

Key Challenges in Implementing Sustainability Reporting

The transition toward climate and sustainability reporting presents several challenges for both public and private sectors. According to Farhana, two critical issues stand out.

Skills and Capacity Constraints

There is a scarcity of professionals who possess expertise in both sustainability and financial reporting.

She emphasised the need for interdisciplinary collaboration, suggesting that organisations may soon require an “ESG controller” to bridge the gap between sustainability and finance functions.

Organisational Clarity on Sustainability Priorities

Another challenge is the lack of clarity regarding material sustainability risks and opportunities. While climate change is often the primary focus, organisations must assess their unique risk profiles to ensure meaningful and relevant disclosures.

Conclusion

Public sector accountants have a pivotal role in driving climate resilience by integrating climate considerations into financial decision-making, risk management, and long-term fiscal planning.

As Governments navigate complex trade-offs in transitioning to a low-emissions and climate-resilient economy, accountants are uniquely positioned to enhance transparency, support evidence-based policies, and strengthen accountability to citizens. Climate-related reporting is ultimately intended to influence behaviour and decision-making. The profession is called upon to move beyond traditional financial reporting and actively contribute to shaping sustainable and resilient public sector governance.

¹ World Metereological Organization, 23 March 2026, State of the Global Climate 2025, https://wmo.int/publication-series/state-of-global-climate/state-of-global-climate-2025

² New Zealand Government, External Reporting Board, https://www.govt.nz/organisations/external-reporting-board/

³ Ministry for the Environment, November 2025, About the Carbon Neutral Government Programme, https://environment.govt.nz/what-government-is-doing/areas-of-work/climate-change/carbon-neutral-government-programme/about-carbon-neutral-government-programme/#about-the-programme