By MIA Professional Practices and Technical

An Initial Public Offering (IPO) is a significant milestone for any company, leading to better brand presence and opportunities, but also introducing a host of new responsibilities as a public listed entity. In Malaysia, 2025 saw a record 60 IPOs on Bursa Malaysia Securities Berhad (Bursa Malaysia), the highest number among the ASEAN exchanges. Against this backdrop of interest in entering the public markets, it is crucial to note that investors are steadily incorporating sustainability considerations into their decision-making, thus recognising that these factors also directly impact business resilience and the long-term value of a company.

This shift is reshaping how prospective IPO companies may be evaluated, with sustainability readiness playing a part in investor decision-making. Malaysia is no exception. With the rollout of the National Sustainability Reporting Framework (NSRF) and the publication of the Securities Commission’s latest Capital Market Masterplan (2026 to 2030), which identifies supporting national sustainability goals as a key strategic outcome theme, sustainability considerations are playing an increasingly prominent role in Malaysia’s capital market landscape.

Alongside Bursa Malaysia’s enhanced disclosure requirements, these initiatives reflect the increasing importance of sustainability considerations within Malaysia’s capital market ecosystem. While sustainability disclosures remain primarily a post-listing obligation, sustainability readiness is likely to become an increasingly relevant aspect of IPO preparation as investor expectations and reporting requirements continue to evolve.

Sustainability Reporting in Malaysia

The commitment to sustainability reporting has strengthened in Malaysia over the years. Bursa Malaysia’s Listing Requirements¹ require listed issuers to include a “Sustainability Statement” in their annual reportscovering material sustainability matters. These requirements were further elevated in 2022 when Bursa announced enhanced sustainability reporting requirements including climate change-related disclosures aligned with the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD).

The advent of the NSRF in 2024 marked the beginning of Malaysia’s next phase in this sustainability journey. By aligning reporting requirements with the IFRS Sustainability Disclosure Standards issued by the International Sustainability Standards Board (ISSB), the NSRF addresses the use of these standards as the baseline for sustainability disclosure, with the aim of ensuring companies provide consistent, comparable and reliable sustainability information that enhances transparency and accountability of how businesses demonstrate sustainability-related risks and opportunities.

International Trends in Sustainability Prospectus Disclosures

Globally, sustainability disclosures in IPO prospectuses are gradually becoming more common, with regulators beginning to incorporate these disclosures directly into prospectus regimes.

In the United Kingdom, the Financial Conduct Authority (FCA) introduced climate-related disclosure requirements² for certain equity issuers if such issuer has identified climate-related risks within its risk factors or climate-related opportunities as material to its prospects as part of its new prospectus regime. Additionally, issuers that have a published climate transition plan are required to include a summary of the plan in the prospectus, as well as details on where it can be located.

In the Asia Pacific region, Hong Kong requires its IPO applicants to put in place necessary mechanisms that enable them to meet the Hong Kong Stock Exchange’s (HKEX) corporate governance and Environmental, Social and Governance (ESG) disclosure requirements upon listing. In its “Guide for New Listing Applicants”³, HKEX requires new applicants to disclose significant ESG-related risks and opportunities, where applicable, in their listing documents.

These developments demonstrate that sustainability is no longer just a post-listing reporting exercise but increasingly a part of the pre-IPO preparation. While the specific approaches may differ across jurisdictions, it is increasingly evident that investors and regulators are expecting IPO-bound companies to demonstrate their readiness on sustainability matters as part of their listing journey.

More broadly, these global developments underscore the growing importance of sustainability considerations in shaping market confidence at the point of listing. For investors, sustainability‑related disclosures provide greater visibility into how issuers identify and manage forward‑looking risks such as climate exposure, supply chain resilience and governance challenges that may affect long‑term performance. As a result, such information is increasingly considered alongside traditional financial disclosures when assessing an issuer’s readiness for public markets.

In the Malaysian context, awareness of international practices is relevant to supporting the quality and credibility of disclosures made by IPO‑bound companies. As sustainability expectations continue to evolve globally, investors may place greater emphasis on governance structures, internal controls, data reliability and sustainability oversight mechanisms disclosed in the prospectus. If regulators were to make such requirements a prerequisite for IPO applicants, this would have practical implications for pre‑IPO planning, the scope of due diligence and the demands placed on finance, risk and reporting functions.

In light of these developments, monitoring international trends is not about replicating other jurisdictions’ regulatory frameworks, but about the market’s strategic positioning and preparedness. Companies and markets that respond proactively to evolving investor expectations are better positioned to build confidence, support valuation discussions and facilitate a smoother transition into post‑listing reporting regimes. This presents Malaysia with the opportunity to strengthen its position on sustainable growth while ensuring its capital market remains competitive in an increasingly sustainability‑focused global environment.

Pre-IPO Considerations and Integration into IPO Strategy

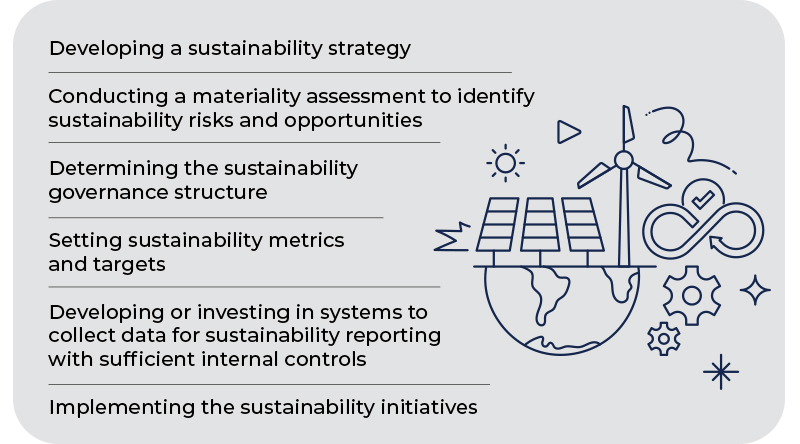

Preparing for an IPO requires companies to demonstrate strong governance, operational efficiency, financial transparency and effective risk management. Today, as sustainability considerations are progressively gaining greater relevance in the context of IPO readiness, companies may also refer to the best practices set out in Bursa Malaysia’s Corporate Governance Guide (CGG), Listing Requirements and Sustainability Reporting Guide. The following are some of the areas companies could focus on:

While all of the above key focus areas are increasingly relevant to IPO readiness, several tend to pose particular challenges for IPO‑bound companies in Malaysia, especially those transitioning from private ownership or founder‑led structures. One of the most common challenges lies in conducting a robust materiality assessment. This requires companies to identify and prioritise sustainability‑related risks and opportunities across their operations and, where relevant, their value chain, supported by appropriate stakeholder engagement. For many companies, particularly those embarking on sustainability reporting for the first time, materiality assessments require greater clarity and structure to support investor understanding.

Another area that frequently proves challenging is the establishment of clear and effective sustainability governance structures. Many private companies lack formalised roles, accountability frameworks and oversight mechanisms for sustainability matters at both board and management levels. Aligning governance arrangements with expectations set out in the CGG and Sustainability Reporting Guide often necessitates changes to board oversight, internal reporting lines and management responsibilities, which take time to embed and operationalise.

In addition, setting meaningful sustainability metrics and targets, together with developing reliable systems and internal controls over sustainability data, can be particularly demanding. Establishing appropriate metrics often requires companies to determine relevant baselines, select suitable measurement methodologies and ensure consistency across business units and time horizons, all of which can be challenging where sustainability data has not previously been tracked in a structured manner. Companies may also face difficulties in calibrating targets that are both achievable and aligned with business strategy, risk appetite and emerging stakeholder expectations, particularly in the absence of established internal benchmarks or historical non‑financial data.

As sustainability information increasingly complements financial information in investor assessments, companies that proactively address the robustness of their metrics, data quality, systems and controls will be better positioned during prospectus preparation and due diligence processes, regardless of whether such requirements are formally mandated for IPO applicants in the future.

Early adoption of these practices can increase the preparedness of IPO-bound companies to navigate post-listing obligations. By integrating sustainability considerations into strategy, governance, risk management and reporting mechanisms during the pre‑IPO phase, companies can build internal capabilities incrementally, strengthen data integrity and address control gaps in a more measured manner. From an IPO readiness perspective, early preparation reduces execution risk, alleviates post‑listing compliance pressure and enables clearer, more credible communication of the company’s sustainability position to investors.

Post-Listing Sustainability Requirements in Malaysia

Upon listing, companies must continue to maintain and strengthen their sustainability practices. Bursa Malaysia requires both Main Market and ACE Market-listed issuers to disclose an annual Sustainability Statement. In 2024, Bursa Malaysia further enhanced its Listing Requirements to align with the NSRF, under which the IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures form the baseline standards for sustainability reporting in Malaysia. Companies that embed sustainability into their governance, strategy, and reporting frameworks before listing will be better placed to meet these obligations after going public.

Opportunities and Challenges

As Malaysia embeds sustainability into its capital markets, IPO-bound companies will face both opportunities and practical challenges.

These opportunities and challenges reflect the current stage of sustainability adoption within Malaysia’s capital markets. As sustainability considerations become more firmly embedded in listing requirements, IPO-bound companies are increasingly preparing to capture the strategic benefits of sustainability readiness while addressing the practical challenges of implementation in anticipation of post-listing obligations. At this stage, sustainability expectations among many companies remain largely compliance‑oriented, with most focused-on understanding and meeting emerging disclosure requirements rather than demonstrating fully embedded sustainability practices across their operations.

For IPO‑bound companies, sustainability readiness is therefore often in its infancy, particularly when compared with larger listed entities that have had more time and resources to develop structured sustainability frameworks, reporting processes and internal capabilities. This represents a natural progression, given that meaningful sustainability integration requires specialist expertise, reliable data, internal ownership and alignment with business strategy elements that are typically built incrementally over time. In addition, governance and oversight mechanisms for sustainability matters are still being formalised, with roles and responsibilities continuing to take shape at both board and management levels. While these foundations are more firmly established among large listed entities, they often form part of broader IPO preparation for companies entering the public markets.

At the same time, these early‑stage considerations present a valuable opportunity to establish the right foundations from the outset. By taking a measured and proportionate approach, focusing on governance clarity, data discipline, internal controls, and alignment with strategy and risk management, IPO‑bound companies can progressively build internal capabilities without undue disruption. Early groundwork allows sustainability considerations to be integrated more seamlessly into reporting, controls and decision‑making processes, rather than being addressed reactively after listing.

Concerns around limited resources, expertise constraints and rising compliance costs are frequently cited, particularly by smaller or newly listed companies. While sustainability readiness does require upfront investment in skills, processes and advisory support, these costs should be considered alongside the longer‑term benefits. Companies that invest early are generally better positioned to reduce execution risk upon listing, respond more efficiently to evolving regulatory expectations, and transition more smoothly to comply with post‑listing requirements.

Ultimately, sustainability readiness for IPO‑bound companies in Malaysia should be viewed not as an immediate expectation to “walk the talk”, but as a process of capability building. Approached strategically and incrementally, sustainability obligations can move beyond compliance to become an enabler of stronger investor confidence, improved access to capital and long‑term value creation, supporting Malaysia’s broader ambition for a resilient and competitive capital market.

Conclusion

As sustainability reporting rises on investor agendas, companies aspiring to take the next step in their growth journey should act early to embed sustainability into their strategies. From the rollout of the NSRF in Malaysia to global developments, the momentum is clear; sustainability readiness is increasingly recognised as an important marker of long-term value and business resilience for any organisation. Companies seeking to list should already be aware of the continuing compliance requirements post-listing. Early action allows sustainability considerations to be embedded thoughtfully into governance, risk management and value creation, rather than being addressed under the pressure of post-listing requirements. In this sense, sustainability readiness is not a last‑minute compliance exercise, but a forward‑looking strategic investment in long‑term resilience and market credibility.

¹ Bursa Malaysia Securities Berhad’s Main Market Listing Requirements and ACE Market Listing Requirements, which include requirements relating to sustainability-related disclosures in annual reports.

² Financial Conduct Authority (FCA) first published the FCA policy statement 25/9 on 15 July 2025 (https://www.fca.org.uk/publications/policy-statements/ps25-9-new-rules-public-offers-admissions-trading-regime)

³ The Guide for New Listing Applicants is published by the HKEX and consolidates all currently effective guidance letters, listing decisions and frequently asked questions related to New Listing. (https://en-rules.hkex.com.hk/rulebook/guide-new-listing-applicants)

This article has been prepared with contributions from the following personnel of Baker Tilly Malaysia and the Malaysian Institute of Accountants (MIA):

- Dato’ Lock Peng Kuan, Managing Partner of Audit and Assurance, Baker Tilly Malaysia;

- Esther Cheah, Partner of Quality Assurance and Technical, Baker Tilly Malaysia;

- Paul Tan, Audit Partner of Transaction Reporting, Baker Tilly Malaysia;

- Mallika Kuppusamy, Associate Director of Quality Assurance and Technical, Baker Tilly Malaysia; and

- Capital Market, Assurance and Practices Department, MIA