By MIA Sustainability, Digital Economy and Services team

MIA has received various accounting queries on leases through our technical queries facility. In this article, we will be sharing a few more common questions received and the suggested guidance for reference.

Previously, we have published several articles on common accounting issues, which can be accessed through the links below:

| 1. MPERS: Common Issues on Consolidation |

| 2. MFRS and MPERS: Common Issues on Investment Property and Property, Plant and Equipment |

| 3. MPERS: Common Issues on Consolidation |

On 27 February 2025, the International Accounting Standards Board (IASB) issued the third edition of IFRS for SMEs Accounting Standard¹. The revised standard will be effective for periods beginning on or after 1 January 2027. In October 2025, the Malaysian Accounting Standards Board (MASB) issued a revised version of Malaysian Private Entities Reporting Standard (MPERS) which aligns with the third edition of IFRS for SMEs Accounting Standard. Accordingly, all MPERS-related guidance set out below is based on MPERS 2025.

Question 1

What is the definition of ‘lease term’?

MFRS

An entity shall determine the lease term as the non-cancellable period of a lease when it consists of both of the following:

- Periods covered by an option to extend the lease if the lease is reasonably certain to exercise that option; and

- Periods covered by an option to terminate the lease if the lease is reasonably certain not to exercise that option.²

An entity will need to assess whether a lessee is reasonably certain to exercise an option to extend a lease, or not to exercise an option to terminate a lease, and an entity shall consider all relevant facts and circumstances as described in paragraphs B37-B40 of MFRS 16.

MPERS 2025³

The term ‘lease term’ is not defined in MPERS (2025) or IFRS for SMEs Accounting Standard.

In the absence of specific guidance in MPERS, a private entity may choose to apply guidance in full MFRS Accounting Standards and those principles do not conflict with requirements in the hierarchy set out in paragraphs 10.4-10.5 of MPERS Section 10 Accounting Policies, Estimates and Errors.⁴

Question 2

What is the accounting treatment for hire purchase interest in suspense for a lessee?

MFRS

Paragraph 26 of MFRS 16 states that “at the commencement date, a lessee shall measure the lease liability at the present value of the lease payments that are not paid at that date. The lease payments shall be discounted using the interest rate implicit in the lease, if that rate can be readily determined. If that rate cannot be readily determined, the lessee shall use the lessee’s incremental borrowing rate”.

The interest rate implicit in the lease is defined as the rate of interest that causes the present value of the lease payments and the unguaranteed residual value to equal the sum of the fair value of the underlying asset and any initial direct costs of the lease.⁵

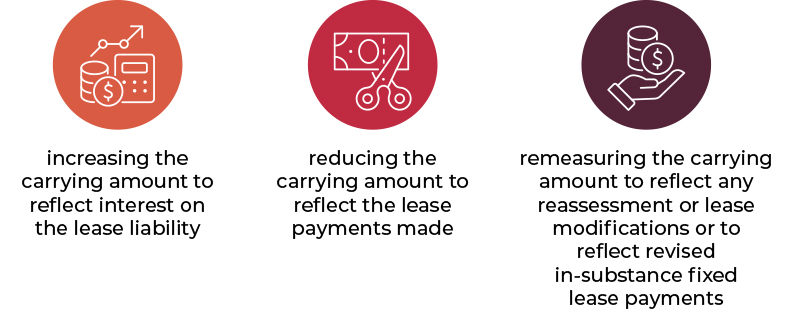

Subsequently, the lease liability shall be measured by:⁶

Interest on the lease liability in each period during the lease term shall be the amount that produces a constant periodic rate of interest on the remaining balance of the lease liability.⁷

MPERS 2025

Paragraph 20.9 of MPERS states that “at the commencement of the lease term, a lessee shall recognise its rights of use and obligations under finance leases as assets and liabilities in its statement of financial position at amounts equal to the fair value of the leased property or, if lower, the present value of the minimum lease payments, determined at the inception of the lease. Any initial direct costs of the lessee (incremental costs that are directly attributable to negotiating and arranging a lease) are added to the amount recognised as an asset”.

The present value of the minimum lease payments should be calculated using the interest rate implicit in the lease. If this rate cannot be determined, the lessee’s incremental borrowing rate should be used instead.⁸

Subsequently, a lessee shall apportion minimum lease payments between the finance charge and the reduction of the outstanding liability using the effective interest method (see paragraphs 11.15-11.20 of MPERS Section 11).⁹

Accordingly, the lease shall be recognised at the amounts equal to the fair value of the leased property or, if lower, the present value of the minimum lease payments at the commencement date, with the finance charge recognised separately over the lease term using the effective interest method.¹⁰

Question 3

A company is involved in property sales and financing activities. Its main sources of income are the sale of properties and the provision of financing services.

The company enters into a “Sale & Purchase Agreement by Rent-to-Own” arrangement for the sale of its properties, whereby ownership of the property will only be transferred to the buyer upon full settlement of the purchase price.

Should this arrangement be classified as a finance lease or an operating lease?

MFRS

Firstly, the entity shall assess whether such an arrangement is or contains a lease. Paragraphs B9 to B31 of MFRS 16 set out guidance on the assessment of whether a contract is, or contains, a lease.¹¹

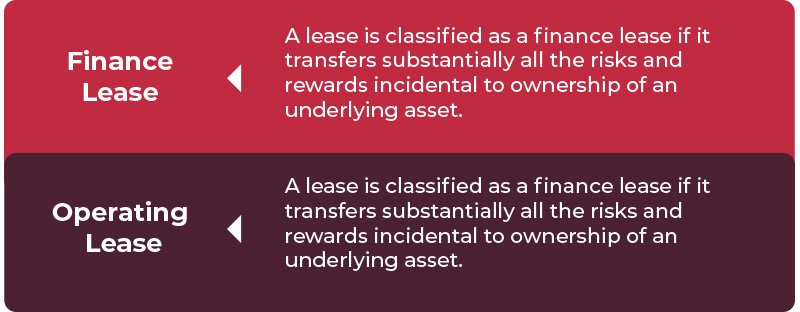

Next, a lessor shall classify the lease as either an operating lease or a finance lease.¹²

Examples of situations that would normally lead to a lease being classified as a finance lease can be viewed in paragraphs 63 of MFRS 16 and the indicators of situations that lead to a lease being classified as a finance lease can be viewed in paragraph 64 of MFRS 16.¹³ Accordingly, the classification of the arrangement depends on whether all the risks and rewards incidental to ownership of the property are transferred substantially to the buyer, rather than merely based on the legal transfer of title.¹⁴

MPERS 2025

An entity shall classify the lease as either an operating lease or a finance lease based on paragraphs 20.4 to 20.8 of MPERS Section 20.

Question 4

A company has a land lease arrangement with a contractual lease period from 23 June 1995 to 22 July 2025.

The lessor and lessee have mutually agreed to extend the lease for another 20 years, commencing from 23 July 2025.

How and when should the depreciation of the additional Right-Of-Use (ROU) asset and the interest expense on the corresponding lease liability be accounted for as a lessee?

MFRS

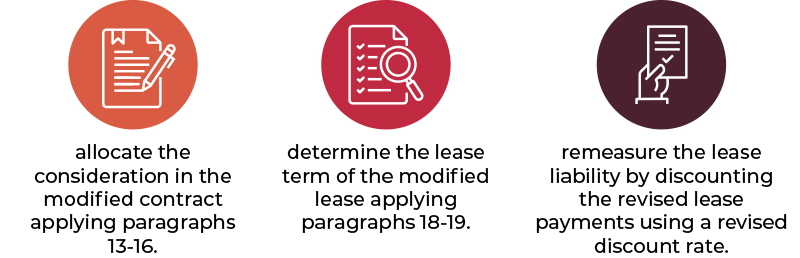

Lease modification is defined as a change in the scope of a lease, or the consideration for a lease, that was not part of the original terms and conditions of the lease (for example, adding or terminating the right to use one or more underlying assets, or extending or shortening the contractual lease term).¹⁵

Firstly, an entity will need to determine whether the lease modification is a separate lease based on paragraph 44 of MFRS 16.

If the lease modification is not accounted as a separate lease, at the effective date of the lease modification, a lessee shall¹⁶:

The remeasurement of the lease liability shall be based on paragraph 46 of MFRS 16. The effective date of the modification shall be the date when both parties agree to a lease modification.¹⁷

MPERS 2025

The term ‘lease modification’ is not defined in MPERS (2025) or IFRS for SMEs Accounting Standard.

However, the private entity shall not anticipate or apply changes made to full MFRS Accounting Standards before the MPERS is amended unless, in the absence of specific guidance in MPERS, a private entity may choose to apply guidance in full MFRS Accounting Standards and those principles do not conflict with requirements in the hierarchy set out in paragraphs 10.4 to 10.5 of MPERS Section 10 Accounting Policies, Estimates and Errors.¹⁸

The views expressed are not the official opinion of MIA, its Council or any of its Boards or Committees. Neither the MIA, its Council or any of its Boards or Committees nor its staff shall be responsible or liable for any claims, losses, damages, costs or expenses arising in any way out of or in connection with any persons relying upon this article.

¹ MIA Accountants Today, September 2025, Overview of the Third Edition of IFRS for SMEs Accounting Standard

² Paragraph 18 of MFRS 16 Leases

³ In October 2025, the Malaysian Accounting Standards Board (MASB) issued a revised version of MPERS which aligns with the third edition of IFRS for SMEs Accounting Standard issued by the International Accounting Standards Board (IASB) in February 2025.

⁴ Paragraph P16 of Preface to the MPERS

⁵ Appendix A Defined Terms of MFRS 16 Leases

⁶ Paragraph 36 of MFRS 16 Leases

⁷ Paragraph 37 of MFRS 16 Leases

⁸ Paragraph 20.10 of MPERS Section 20 Leases

⁹ Paragraph 20.11 of MPERS Section 20 Leases

¹⁰ Paragraphs 20.9 and 20.11 of MPERS Section 20 Leases

¹¹ Paragraph 9 of MFRS 16 Leases

¹² Paragraph 61 of MFRS 16 Leases

¹³ Paragraphs 63 and 64 of MFRS 16 Leases

¹⁴ Paragraph B45 of MFRS 16 Leases

¹⁵ Appendix A Defined Tems of MFRS 16 Leases

¹⁶ Paragraph 45 of MFRS 16 Leases

¹⁷ Appendix A Defined Tems of MFRS 16 Leases

¹⁸ Paragraph P15 of Preface to the MPERS