By Chong Mun Yew & Dr. Voon Yuen Hoong

In Malaysia, the role of Independent Non‑Executive Directors (INEDs) has grown increasingly significant as public-listed companies reinforce their commitment to corporate governance, board independence, and accountability. Although INEDs are not involved in the daily management of a company, they provide crucial oversight, strategic direction, and objective scrutiny of management actions. As regulatory expectations evolve and board responsibilities intensify, the structure of INED remuneration — comprising directors’ fees, meeting allowances and various benefits — has become increasingly diverse and complex.

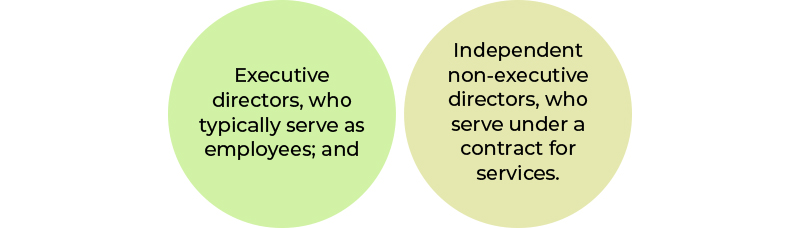

Given this development, the tax treatment of remuneration paid to INEDs has attracted growing attention from companies, directors, and tax practitioners. Traditionally, directors’ fees were categorised as employment income subject to Monthly Tax Deductions (MTD). However, unlike executive directors, who typically serve as employees of the company, INEDs often fall within a different tax classification. This distinction influences on how their income is assessed and reported, raising important compliance considerations under Malaysia’s income tax regime. Key issues include the proper characterisation of income, the timing of tax liabilities, and the compliance obligations imposed on companies that remunerate INEDs.

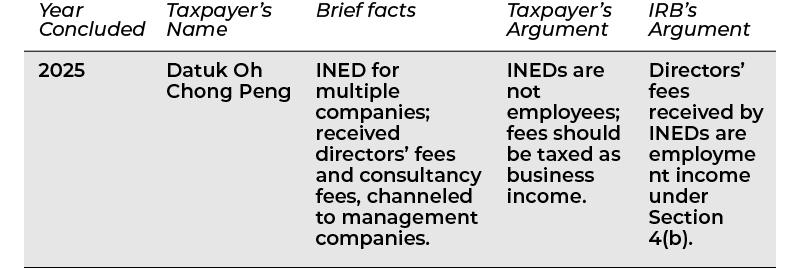

A central question is whether INED remuneration should be taxed as employment income under Section 4(b) of the Income Tax Act 1967 (ITA) or as business income under Section 4(a). This issue came under judicial scrutiny in the landmark case of Datuk Oh Chong Peng v Ketua Pengarah Hasil Dalam Negeri (KPHDN), decided by the Court of Appeal (COA) in October 2025. The case involved determining whether INED fees, meeting allowances, and consultancy fees received by Datuk Oh constituted employment income or business income. The decision of the High Court and the COA differed from that of the Special Commissioners of Income Tax (SCIT), prompting a judicial clarification with far‑reaching implications.

Background: The Case of Datuk Oh Chong Peng v KPHDN

Facts of the Case

Datuk Oh served as an INED on the boards of 7 to 8 public companies between the Years of Assessment (YAs) 2002 to 2012 following his retirement from professional practice. To manage his professional engagements, he established two management companies — OCP Holding Sdn Bhd and Garzania Sdn Bhd – to which he channelled all directors’ fees, meeting allowances, and consultancy fees. In addition to his directorships, he occasionally provided consultancy services to other companies.

The income channelled to the management companies was treated as business income, and in turn, the companies paid Datuk Oh a monthly salary, which he also declared as income under Section 4(a). This arrangement had been consistently applied since 1998 and accepted by the Director General of Inland Revenue (DGIR) until 2015.

Following a tax audit, however, the DGIR reclassified the directors’ fees and allowances as employment income, issued additional tax assessments for YAs 2002 to 2012, and imposed penalties. The DGIR argued that the remuneration constituted income derived from Datuk Oh’s personal service as a director of the companies.

SCIT Decision

Datuk Oh appealed to the Special Commissioners of Income Tax (SCIT), but the SCIT dismissed his appeal. The SCIT held that:

- he was an employee,

- the remuneration was employment income, and

- EA forms issued by public companies constituted prima facie evidence of an employment relationship.

This conclusion was reached despite the fact that Datuk Oh did not receive typical employee benefits such as Employees Provident Fund (EPF) or Social Security Organisation (SOCSO) contributions from the companies on whose boards he served.

High Court Decision

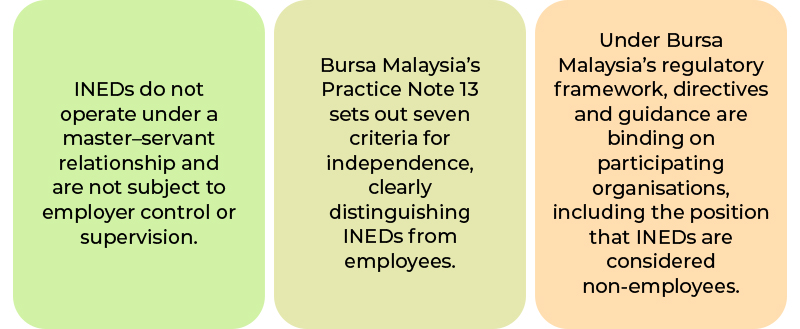

On further appeal, the High Court overturned the SCIT’s decision. The Court held that INEDs are not employees for tax purposes and that fees paid to INEDs should be taxed as business income under Section 4(a). In reaching this conclusion, the High Court noted:

The High Court also found that the SCIT had failed to properly analyse the nature of the relationship between Datuk Oh and the public companies.

Court of Appeal Decision (October 2025)

The Court of Appeal (COA) upheld the High Court’s judgment, confirming that income earned as an INED should be treated as business income. A three‑member panel led by Justice Datuk Collin Lawrence Sequerah emphasised the clear distinction between:

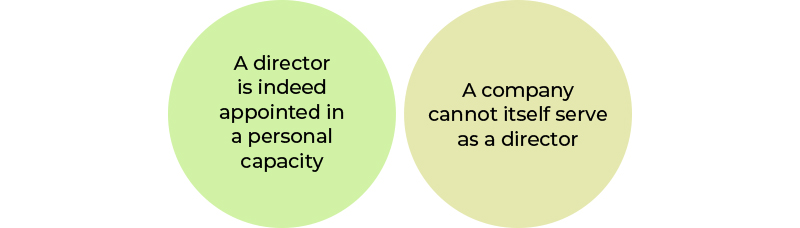

During the appeal, the Inland Revenue Board (IRB) questioned whether the remuneration was genuinely attributable to Datuk Oh’s personal services, given that the fees were channelled to his management companies in view of the following reasons:

However, the tax classification depends not on appointment mechanics, but on the nature of the relationship between the director and the company.

Since no master – servant relationship existed, and because Datuk Oh was not subject to the control of the companies, the director’s fees were rightly treated as business income.

Summary of Case Outcomes

Practical Tax Implications for INEDs and Public Companies

The Court of Appeal’s decision has significant implications for how public companies and INEDs must handle remuneration, reporting, and compliance matters.

(i) Tax Filing Requirements

Following the decision:

- INEDs must declare directors’ fees as business income and not employment income.

- Their tax filing deadline typically moves from April to June, as business income earners are using Form B. A grace period for e-filing until 15 July for YA 2025, based on the Return Filing Programme issued by the IRB dated 30 December 2025.

- INEDs may claim allowable business deductions under Section 33(1) of the ITA, including:

- professional fees,

- travel expenses,

- meals incurred during official duties, and

- other expenses which are wholly and exclusively incurred to produce income.

This may offer potential tax efficiency depending on the INED’s allowable expense claims.

(ii) Notice of Instalment Payment (Form CP500)

Form CP500 is a notice of instalment payment issued by the IRB for individuals earning non-employment income (e.g. freelance, business, or rental income). It allows taxpayers to settle their tax liabilities in six bi-monthly instalments instead of a lump sum.

Payments are made once every two months, starting in March and ending in January of the following year.

Revisions can be made via Form CP502:

- The first revision must be submitted no later than 30 June; and

- The second revision must be submitted no later than 31 October each calendar year.

(iii) E‑Invoicing Compliance

Since the relationship between INEDs and public companies is contractual rather than employment‑based:

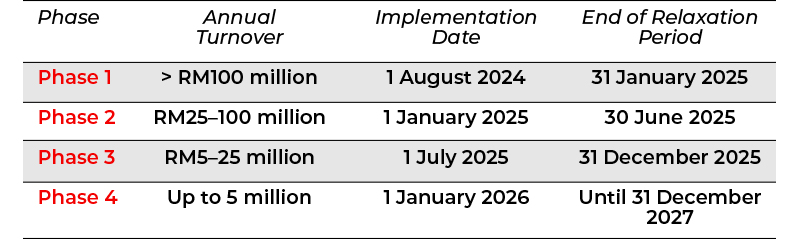

- INEDs must issue validated e‑Invoices to public-listed companies for directors’ fees and related remuneration once the relevant threshold has been exceeded i.e., above RM1 million but not exceeding RM5 million, the implementation date for which was on 1 January 2026.

Above is the latest timeline for e-Invoicing implementation in Malaysia, updated as of 20 April 2026, by the Inland Revenue Board of Malaysia (IRBM)

- Based on the e-Invoicing guidelines issued on 5 May 2026, the 6-month interim relaxation period for taxpayers with an annual turnover of up to RM5 million has been extended to 31 December 2027. Taxpayers with annual turnover below RM1,000,000 are exempted from e-Invoice implementation.

- E-Invoicing obligations in Malaysia are determined based on annual turnover assessed on a rolling 12-month basis, against the RM1 million exemption threshold. Once revenue exceeds this threshold during any continuous 12-month period, e-Invoicing becomes mandatory on 1 January of the second immediate year.

- INEDs are classified as individuals carrying out business activities for tax purposes.

- Companies must capture, validate, and document these invoices within their procurement or accounts payable systems.

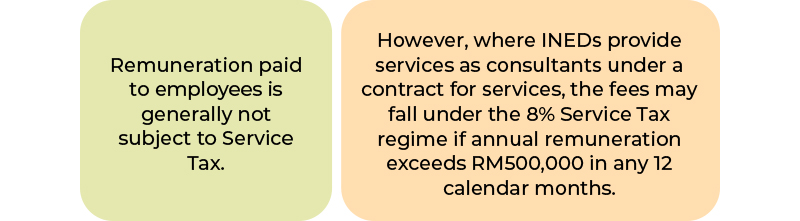

(iv) Service Tax Considerations

A key implication relates to Service Tax:

- INEDs who exceed the threshold must:

- register for Service Tax,

- charge Service Tax where applicable, and

- submit bi‑monthly Service Tax returns to the Royal Malaysian Customs Department (RMCD).

Companies must accordingly distinguish between employees and service providers when processing directors’ fees.

Precautionary Measures Before a Tax Audit

Given that INED remuneration is now treated as business income, INEDs must adopt appropriate compliance practices. Key precautions include:

1. Maintain Proper Records

INEDs should keep complete and accurate records supporting expense claims, including receipts, invoices, appointment letters, meeting schedules, and correspondence.

2. Prepare Full Sets of Accounts

As business income earners, INEDs must prepare full sets of accounts for submission, including statements of income and expenses.

3. Adhere to Tax and Regulatory Deadlines

Compliance with deadlines for income tax filings, service tax submissions, and e‑Invoicing validation is essential to avoid penalties.

4. Incorrect application of Monthly Tax Deduction (MTD)

A common issue among Malaysian public-listed companies is the incorrect application of MTD on remuneration paid to INEDs.

Under Malaysian tax regulations, directors’ fees and certain forms of directors’ remuneration are generally subject to specific withholding and reporting requirements that differ from those applicable to regular employment income. However, many public-listed companies continue to process payments to INEDs through the normal payroll system and apply MTD as if the directors were employees.

This practice may result in inaccurate tax deductions, incorrect payroll reporting, and potential non-compliance with the requirements of the IRB. Public-listed companies should carefully review the nature of the remuneration paid to INEDs and ensure that the appropriate tax treatment is applied.

5. Exercise Caution in Using Management Companies

While structuring activities through management companies may provide flexibility, such arrangements must comply with anti‑avoidance provisions. Poorly substantiated or artificial arrangements may draw scrutiny and lead to penalties.

6. Understand the Risk of Non‑Compliance

Failure to comply with tax obligations can result in:

- penalties,

- additional assessments,

- heightened audit risk, and

- disputes with tax authorities.

Conclusion

A summary of the Datuk Oh’s court case is provided below:

The Datuk Oh Chong Peng ruling has clarified that INED remuneration in Malaysia should be treated as business income. The courts held that directors’ fees and allowances received by INEDs do not constitute employment income under Section 4(b) of the ITA as INEDs are not engaged under a contract of service and are required to exercise independent oversight over management. Accordingly, such remuneration falls within Section 4(a) of the ITA as business income.

By contrast, consultancy fees must be evaluated based on the nature of the underlying relationship. Where consultancy services are rendered pursuant to a contract of service which gives rise to an employer-employee relationship, the remuneration would generally be taxable under Section 4(b) as employment income. Conversely, where the consultancy services are provided independently in the course of carrying on a profession, vocation or business, the fees would ordinarily fall within Section 4(a) as business income.

The judgment underscores that the proper characterisation of income depending on the legal relationship between the parties and the capacity in which the services are performed, rather than the title or description of the payment.

This re-characterisation of INED remuneration as business income also raises consequential questions under the Service Tax framework. Where an individual director is regarded as carrying on a business activity and exceeds the prescribed registration threshold for taxable services, consideration may need to be given as to whether the provision of directorship services constitutes a taxable service for Service Tax purposes. This issue has gained prominence following the expansion of the Service Tax regime effective 1 July 2025, which broadened the tax base and increased compliance obligations across various service sectors.

Overall, the decision significantly affects how INEDs file taxes, claim deductions, and comply with Service Tax and e‑Invoicing requirements. With increased scrutiny from tax authorities and heightened governance expectations, both companies and INEDs must ensure they understand the practical implications and maintain strong compliance practices.

As remuneration structures continue to evolve, it is essential for public-listed companies and their INEDs to reassess remuneration arrangements, payroll practices, tax reporting positions, and invoicing processes to align with the evolving regulatory landscape. Further guidance from both the IRB and the RMCD would be beneficial in clarifying the interaction between income tax, Service Tax, and e-Invoicing requirements arising from the Datuk Oh Chong Peng’s court case decision.

Chong Mun Yew & Dr. Voon Yuen Hoong are Tax Partners under Crowe Malaysia PLT.

The content in this article is the personal view of the authors and does not purport to reflect the views of Crowe Malaysia PLT or the Malaysian Institute of Accountants.